Sell-Side vs Buy-Side Representation in 2026: Which Is Right for California Lower-Middle-Market Owners?

Sell-Side vs Buy-Side Representation

By Andrew Rogerson, CM&AP, LCBB (Rogerson Business Services).

Andrew Rogerson is an M&A advisor and a 35+ year business owner who helps California lower and mid-market owners value, position, and sell their companies through sell-side representation. Credentials:CM&AP and LCBB listing.

You’re getting ready to exit in the next 6–24 months and want to avoid underselling. Here’s the short answer: if your goal is to maximize valuation while protecting confidentiality, a disciplined sell-side representation is usually the right fit. Buy-side representation is built for acquirers who need sourcing and price discipline. The rest of this guide shows the differences, California nuances, and when each path wins.

Timing matters because a large share of U.S. business owners skew older. The U.S. Census Bureau notes that over half of U.S. business owners were age 55+ (Annual Business Survey; see“Business Owners’ Ages” visualization). In California, that demographic reality often shows up as more owners running a process on a tighter clock—sometimes after an unsolicited offer lands.

Guide Context

For context on who this guide is written for: Rogerson Business Services’ ideal client is a California business owner planning an exit or sale, typically with $2 million to $50 million in annual revenue, in industries such as manufacturing, construction, managed IT services, industrial services, business services, healthcare, logistics and transportation, and wholesale distribution.

This guide is also informed by the perspective of Andrew Rogerson—a California M&A advisor with 20+ years in the market and credentials including Certified Mergers & Acquisition Professional (CM&AP)—see the firm’s About page.

Let’s dig in.

Key takeaways

- If you’re a California owner planning to sell in the next 6–24 months, sell-side representation is usually designed to maximize price and terms by creating competitive tension.

- If you’re an acquirer building a pipeline (or trying to avoid overpaying), buy-side representation is built around sourcing, screening, and diligence depth.

- The practical “right” answer often comes down to confidentiality needs, diligence readiness (QoE/data room), and whether you want an auction or a discreet, limited process.

Side-by-Side Comparison of sell-side vs buy-side representation

The table below compares core dimensions sellers ask about most. Structure is parity-based for fairness and clarity.

Tip: Read the table like a checklist. If you’re a seller, prioritize the rows tied to price/terms (process design, diligence readiness, confidentiality, and outcome quality). If you’re a buyer, prioritize fit and risk (sourcing depth, diligence depth, and integration planning).

| Dimension | Sell-Side Representation | Buy-Side Representation |

|---|---|---|

| Quick verdict (best for) | Owners planning to sell within 6–24 months who want competitive tension, strong terms, and tight confidentiality. | Acquirers building a pipeline of targets and enforcing price/fit discipline over a longer horizon. |

| Objectives and incentives | Create a market, maximize price and terms, and close with high certainty; compensation typically scales with value realized. Definitions align with advisor roles described by DealRoom’s overview of mandates (2026). See the explanation of mandate scopes in the DealRoom sell-side vs buy-side overview. | Source, evaluate, and acquire at a compelling price/structure; compensation often mixes retainers with smaller contingent fees, rewarding disciplined execution and fit. |

| Process and market reach / sourcing depth | Curated buyer universe, controlled outreach, credentialed CIM, management meetings, and a two-round process to drive stronger bids. Education-grade process outlines match the phases summarized by Wall Street Prep’s sell-side process. | Systematic mapping of target lattice (industry, size, geography), off-market sourcing, management access, and iterative evaluation to find value and strategic fit. |

| Diligence readiness vs diligence depth | Emphasis on pre-market QoE, data-room hygiene, defensible add-backs, and staged disclosures to reduce retrades and busted LOIs. For valuation preparation, see California guidance in How to Value a Business for Sale in California. | For buyers, deep financial, commercial, legal, and operational diligence to avoid overpaying or inheriting problem assets; heavy use of third-party experts. |

| Confidentiality controls | Code-named outreach, NDAs, strict VDR permissions/audits, and planned employee/customer communications; aligns with CPRA-aware information handling. Statutory text is consolidated in the California CPRA statute. | Similar NDA/VDR discipline, though more people may be involved across the buyer’s team and advisors; access expands as diligence deepens. |

| Outcome quality (price, terms, certainty) | Competitive dynamics can raise price and improve terms. Multiple studies show auctions tend to outperform one-to-one talks; for example, an HBS/SSRN paper (updated 2021) found roughly 4–7% higher prices overall, with larger gains for private targets; see the research summarized in Auctions vs. Negotiations in M&A. | Better fit and synergy capture for the buyer; disciplined sourcing and valuation frameworks help avoid overpaying, though there’s no inherent mechanism to raise the seller’s price. |

| Timeline to LOI / close (as of 2026) | Typical lower middle market sale runs ~6–9 months end-to-end with solid preparation. Phase guidance: outreach to LOI often 8–12 weeks; post-LOI to close ~60–90+ days depending on financing and approvals. See phase context in Wall Street Prep’s sell-side process. | Acquisition timelines vary widely; buyers often operate continuously. A single buy-side deal may take several months from first contact to close, especially if sourcing off-market targets and arranging financing. |

| Cost to client (as of 2026; varies) | Directionally: a work/retainer fee plus a success fee that scales with enterprise value (Lehman-style variants). For current survey-based snapshots of sell-side fees, see the Firmex Global M&A Fee Guide 2024–2025. | Often a monthly retainer and smaller success fee relative to sell-side mandates. Public, survey-grade buy-side fee ranges are limited; expect proposals to vary by scope, sector, and deal size. |

| California specifics | Expect escrow-driven closing mechanics, potential sales tax on tangible assets, and capital gains taxed at ordinary CA rates. Coordinate early with your CPA and counsel. Practical escrow context appears in Rogerson’s Escrow Process in California When Selling Your Business. | For buyers, CPRA-aware data handling, licensing/permits transitions, and lender diligence can extend timing; integration planning is critical to protect value post-close. |

| Buyer universe access vs integration planning | Sell-side advisors curate strategic and financial buyers in relevant sectors and geographies to maximize competition and fit. | Buy-side teams develop integration theses and day-one plans to capture synergies and reduce value leakage after close. |

| Conflict management and fiduciary posture | Clear engagement terms, exclusivity during marketing, and avoidance of dual-representation conflicts; disclosures on fees and marketing scope. | Buy-side advisors should disclose any target-side relationships, avoid undisclosed dual roles, and clarify success metrics and sourcing methods. |

| Typical use cases | Full or limited auction, unsolicited offer defense, discreet bilateral with negotiation support, carve-outs, management buyouts with competitive tension. | Programmatic roll-up, add-on sourcing, proprietary off-market outreach, competitive bid participation with valuation guardrails. |

Don't have time to read more?

Take a shortcut and play the video overview below

Which Should You Choose? Real California Scenarios

Every exit is different. Think of these as realistic snapshots to help you map your situation to the right mandate.

Tip: If you’re torn between a full auction and a limited process, don’t decide based on “how many buyers” you want—decide based on what risk you’re managing. Concentration risk and weaker reporting often benefit from more competitive tension (with staged disclosures), while extreme confidentiality constraints can favor a tighter, credentialed buyer set.

Real deal example, California anonymized

In one lower middle market manufacturing sale (company name redacted), negotiations began in early November 2020, and the transaction ultimately closed in mid-September 2021. The escrow process was unusually difficult, with four separate attempts to close the sale (each about a week apart).

“I think three important pieces are: One, be prepared for the unexpected, and two, learn from your advisors as they have the experience of having done this before, and three, make the best decisions you can with what you know.” — Andrew Rogerson, sell-side advisor

“It was an emotional roller coaster. Not to be repeated in a hurry.” — Seller (anonymized)

Read the full case study: How RBS Advisors Sold a Lower Middle Market Manufacturing Business Worth $36 Million.

Seller feedback after closing, California anonymized

After escrow closed on a California landscaping business sale (company name redacted), the sellers emphasized that what mattered most was steady communication and guidance through obstacles:

“We are very satisfied with the entire process of selling our business. Although it was long and we encountered many challenges, you took the time to explain the issues to us as they came with integrity, patience, and you did so promptly… We would confidently recommend your services to anyone looking to sell or buy a business in the area you cover.” — Seller (anonymized)

Read the full case study: How RBS Advisory Firm Sold a California Landscaping Business Quickly.

- Industrial distributor, Central Valley, owner 62, top three customers = 58% of revenue. Recommended: sell-side representation with a limited auction. Why it fits: a curated set of strategic and financial buyers can price concentration risk more intelligently if they see clean QoE, tight customer retention data, and a well-argued working capital peg. The auction dynamic helps defend valuation while controlling disclosures. If you’re still modeling value, review California-focused guidance in the internal primer How to Value a Business for Sale in California.

- Bay Area medical practice, owner 57, compliance-sensitive data, and staff stability concerns. Recommended: sell-side representation with staged VDR access and specialized counsel. Why it fits: confidentiality-forward NDAs and CPRA-aware access controls minimize leak risk; a controlled process vets buyers for credentialing and post-close continuity. Keep patient and staff data locked down until late-stage diligence per the California CPRA statute.

- Business with attached real property, Southern California. Recommended: sell-side representation coordinating escrow, property diligence, and potential SBA/credit timelines. Why it fits: Combining a business sale with real estate adds steps and stakeholders. California escrow norms, lender timing, and tax allocations are easier to manage with a single quarterback. For process context, see the internal explainer Escrow Process in California When Selling Your Business. If you’re in construction or related trades, you may also find the sector guide useful: Selling a Construction Company in California.

Fees and Timelines in 2026 — What to Expect

Fees vary by deal size, complexity, and scope, so treat the following as directional snapshots rather than quotes.

Tip: If you want to avoid valuation “give-backs” later, focus less on the initial headline price and more on what drives the final number: QoE-ready financials, defensible add-backs, and a clear working capital target (the working capital peg). Those three items often determine whether you get a retrade post-LOI.

A quick translation of those terms: a working capital peg is the “normal” level of net working capital the buyer expects the business to deliver at closing (think: enough AR, inventory, and cash—net of payables—to run the business without a cash squeeze).

If you close below the peg, the purchase price is often reduced dollar-for-dollar; if you close above it, you may be paid more—so agreeing on what “normal” means early can prevent surprises. Add-backs are adjustments that increase reported earnings (and can increase valuation), but they need to be documented and repeatable—one-time expenses, owner perks, or non-recurring events are easier to defend than vague “miscellaneous” items.

A seller-side Quality of Earnings review pressure-tests these points (revenue quality, margin sustainability, customer concentration, and normalization adjustments) so you’re less likely to face a late retrade after the LOI.

A few California-specific facts to keep in mind as you plan:

- State taxes can change net proceeds. California taxes capital gains at ordinary state income rates, so structure and timing matter (coordinate with your CPA).

- Escrow is often central to closing mechanics. California deals frequently use escrow-driven steps and document choreography, which can add time and stakeholders.

- Asset sales can carry sales-tax and allocation implications. When a transaction includes tangible assets (FF&E/inventory), tax and purchase-price allocation questions can show up early in diligence—plan for them.

- Sell-side fees. Lower middle market engagements commonly combine a work/retainer fee with a success fee that scales down as enterprise value rises (Lehman-style variants). For a contemporary survey-based context, review the Firmex Global M&A Fee Guide 2024–2025. Ask advisors to show you the fee math at a few price points so you can compare apples-to-apples.

- Buy-side fees. Public, survey-grade ranges are sparse. Expect a monthly retainer and smaller contingent fees than sell-side. Because the buy-side scope can span months of sourcing and diligence, request detailed proposal assumptions and milestones.

- Timeline. With solid preparation, many California lower middle market sales run ~6–9 months from kickoff to close. Education-grade outlines of the sell-side phases are summarized by Wall Street Prep’s sell-side process. California escrow steps, lender diligence, and regulatory reviews can extend or compress timing. To understand escrow’s role in local closings, skim the internal guide Escrow Process in California When Selling Your Business.

- Taxes. California taxes capital gains at ordinary state income rates; plan early with your CPA. For background, Rogerson’s overview of capital gains provides context you can discuss with your tax team: Is Selling a Business Considered Capital Gains in California?. Nothing here is tax advice—coordinate decisions with your CPA and counsel.

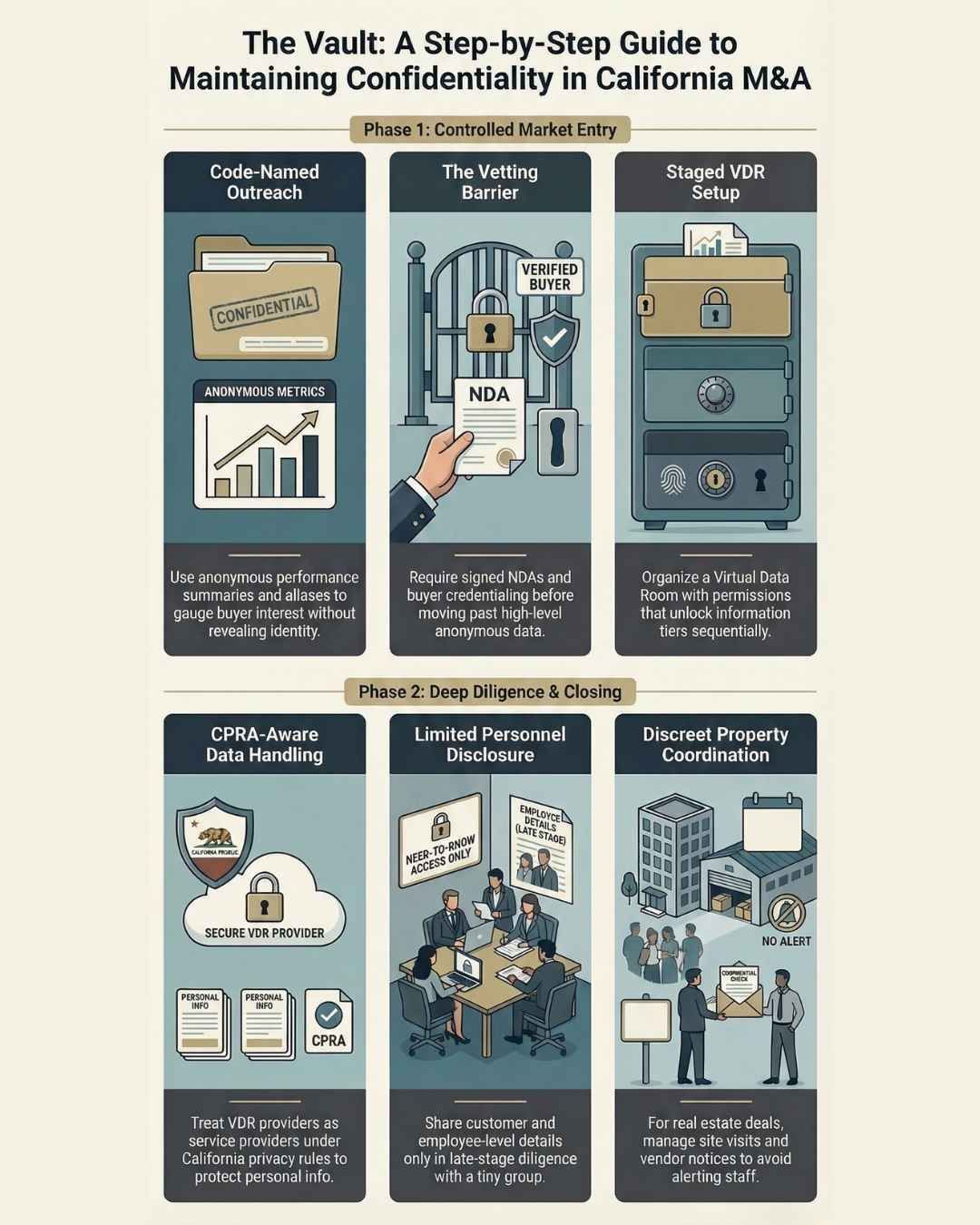

How Confidentiality Stays Tight in California

A confidentiality-forward sell-side process uses code names, tailored NDAs, staged VDR access, and precise communications planning so staff and customers aren’t surprised.

Tip: Treat confidentiality like a phased funnel: share anonymous performance summaries early, customer-level and employee-level detail only after buyer credentialing, and personal information (if needed at all) as late as possible—and only to the smallest necessary group. That includes restricting personal information, logging access, and treating your VDR provider as a service provider under California privacy rules. For statutory framing, see the consolidated California CPRA statute. If you’re selling a company with attached real property, there are added sensitivities around site visits, environmental records, and vendor notices; Rogerson’s resource on combined transactions offers practical context: Sell Commercial Property With Operating Business In California.

FAQs

Tip: Before you talk to any advisor, come prepared with (1) the last 3 years of financial statements and a clean trailing-twelve-month view, (2) your best list of add-backs, (3) a customer concentration summary, and (4) your “who can know what, when” confidentiality plan. Those four items drive both valuation and process design.

Disclosure: This article is for general information only and isn’t legal, tax, or financial advice. Deal terms, taxes, and timelines depend on your facts—review decisions with your CPA and legal counsel. If an advisor is ever asked to support more than one party in a transaction, that should be handled only with clear conflict disclosures and written consent by the parties. Content reviewed for 2026 market context.

What’s the core difference between sell-side vs buy-side representation?

Sell-side is hired by the owner to create a market, maximize valuation and terms, and close with certainty. Buy-side is hired by an acquirer to source targets, evaluate fit, and avoid overpaying. A concise mandate overview appears in the Lower Millde Market at Rogerson Business Services sell-side vs buy-side explainer.

Which path maximizes my sale price as a seller?

In most seller situations, a disciplined sell-side auction or limited auction is best. Academic evidence (updated 2021) indicates that auctions tend to achieve higher prices than one-to-one negotiations; see the summary in Auctions vs. Negotiations in M&A. Results vary with preparation quality and buyer universe.

How long will a California lower middle market sale take?

Many deals are completed in ~6–9 months with strong preparation. Outreach-to-LOI often runs 8–12 weeks, and LOI-to-close ~60–90+ days depending on financing and approvals. For phase context, review Rogerson Business Services Prep’s sell-side process. California escrow and lender steps can shift timing.

How do fees typically work in 2026?

Sell-side: a work/retainer component plus a success fee that scales with enterprise value. Survey-based snapshots are compiled in the Firmex Global M&A Fee Guide 2024–2025. Buy-side: often a monthly retainer plus smaller contingent fees; public survey ranges are limited, so compare proposals carefully.

Should I hire sell-side help if I already have an interested buyer?

Often yes, but scope it appropriately. A limited-scope sell-side mandate can preserve confidentiality, test price with a small set of alternates, and negotiate terms, reps, and warranties, and the working capital peg—without running a wide auction.

Also consider this: if you want help running a California sell-side process, look for an advisor who can (1) build a buyer universe that fits your industry, (2) manage confidentiality with staged disclosures, and (3) help you get diligence-ready (QoE, defensible add-backs, and a clear working capital target) so you don’t give value back late in the deal. Rogerson Business Services is one example of a California-focused sell-side advisory firm; you can review its resources and case studies at Rogerson Business Services.

Hey there! Can we send you a gift?

We just wanted to say hi and thanks for stopping by our little corner of the web. :) we'd love to offer you a cup of coffee/tea, but, alas, this is the Internet.

However, we think you'll love our email newsletter about building value and properly position your company before transition/exit your business ownership.

As a special welcome gift for subscribing, you'll also get our helping and educational guides, tips, tutorials, etc.. for free.

It's filled with the best practices for retiring serial business owners like Dan Gilbert, Larry Ellison, Warren Buffett, and many more.

Just sign up for our emails below.