Earnout vs Seller Financing (2026): Which Is Faster and Lower Risk for California Sellers?

Earnout vs Seller Financing: Which is Better?

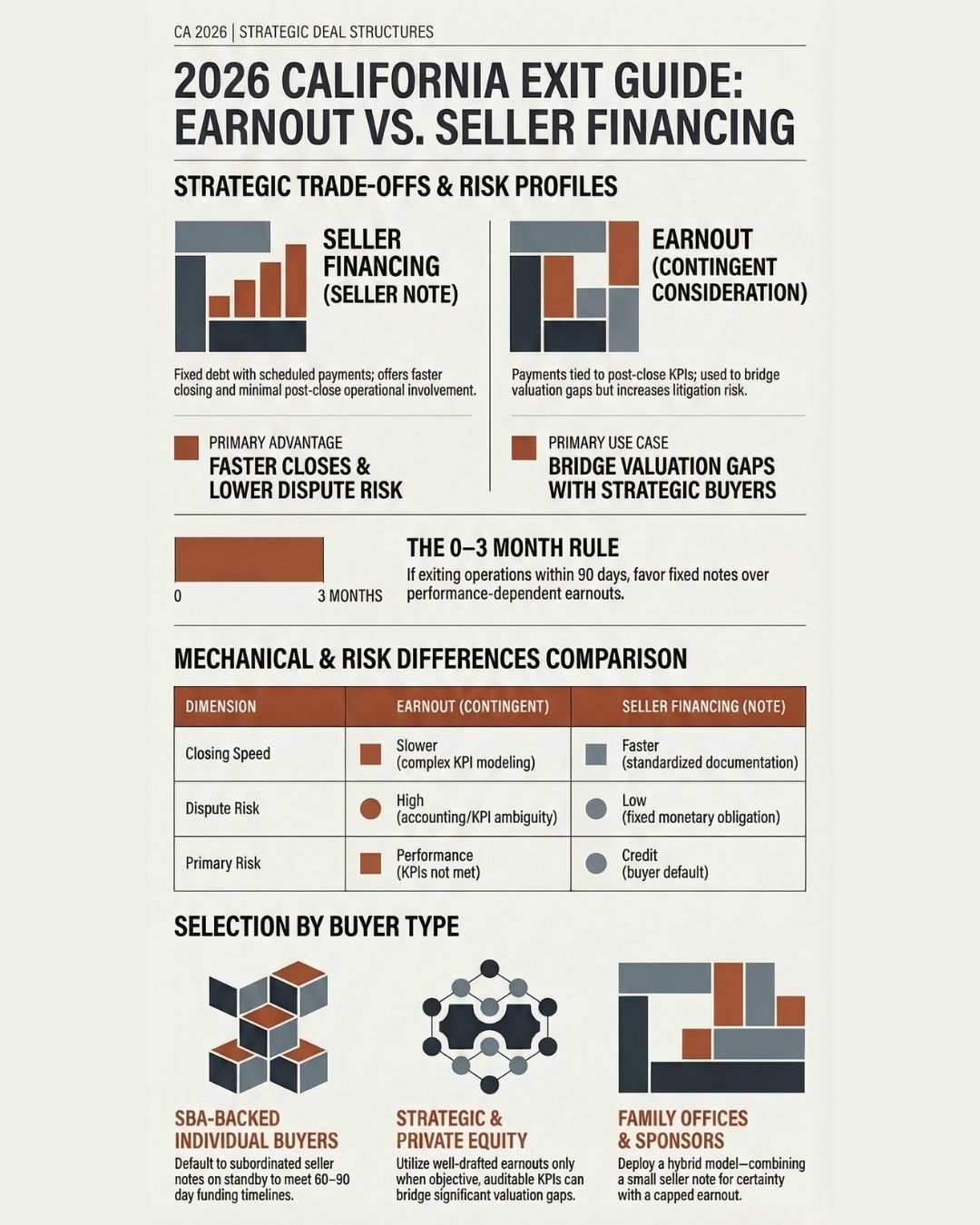

If you’re selling a California lower middle market company and want speed to close with minimal post‑close involvement, here’s the quick verdict: a straightforward seller note (properly subordinated—and on SBA‑compliant standby if applicable) generally closes faster and with fewer disputes than a KPI‑based earnout.

Use an earnout selectively when you truly need to bridge a valuation gap and the KPI is objective, auditable, and insulated from buyer‑driven changes. For a broader process context, see the California‑focused walkthrough in Walk Me Through A Sell Side M&A Deal.

Guide Context

For context on who this guide is written for: Rogerson Business Services’ ideal client is a California business owner planning an exit or sale, typically with $2 million to $50 million in annual revenue, in industries such as manufacturing, construction, managed IT services, industrial services, business services, healthcare, logistics and transportation, and wholesale distribution.

This guide is also informed by the perspective of Andrew Rogerson—a California M&A advisor with 20+ years in the market and credentials including Certified Mergers & Acquisition Professional (CM&AP)—see the firm’s About page.

Let’s dig in.

Key takeaways

- If speed to close and low dispute risk are the priority, favor a seller note over a KPI-based earnout—especially when you expect to step back within 0–3 months.

- For SBA-backed buyers, the practical path is usually a lender-approved, fully subordinated seller note on standby. Confirm the lender’s current requirements before you sign.

- Use an earnout only to bridge a real valuation gap—and only when the KPI is objective, auditable, and protected from buyer-driven changes.

- Match the risk you’re taking to the protection you get: seller notes are primarily credit risk (mitigate with security/guarantees where possible), while earnouts are performance and interpretation risk (mitigate with precise definitions, audit rights, and dispute resolution).

Fun fact (California deal dynamics): In many lower middle market deals, the “faster close” isn’t usually about drafting speed—it’s about how many third parties have to sign off (lenders, landlords, and sometimes licensing agencies). That’s one reason simpler, lender-friendly terms tend to move quicker.

Side‑by‑Side: Earnout vs Seller Financing

Below is a practical comparison tailored to California sellers prioritizing a clean, lower‑risk process and minimal post‑close involvement (0–3 months). Terms are market‑dependent and should be confirmed at signing as of 2026‑03‑05.

Don't have time to read more?

Take a shortcut and play the video overview below

| Dimension | Earnout (Contingent Consideration) | Seller Financing (Seller Note) |

|---|---|---|

| Mechanics | Deferred, contingent payments tied to post‑close KPIs (e.g., revenue/EBITDA). Requires tight definitions, measurement periods, and audit rights. | Fixed promissory note with scheduled payments and stated interest; typically subordinated to senior/SBA debt and may be on standby. |

| Cash at Close Certainty | Usually lowers cash at close to protect buyer downside; total proceeds uncertain until KPIs are measured. | Often enables more cash at close vs. an earnout because the remaining portion is fixed debt rather than contingent. |

| Post‑Close Seller Involvement | Often assumes seller has influence over KPI drivers; with 0–3 months of involvement, risk of underperformance rises. | Minimal operational involvement; obligations are primarily financial (note servicing), not managerial. |

| Dispute/Litigation Risk | Higher risk around KPI definitions, adjustments, and accounting policies; mitigated by precise drafting and audit rights. | Lower computational ambiguity; risk centers on buyer creditworthiness and subordination/standby restrictions. |

| Financing Dependency & SBA Fit | Contingent payouts can complicate lender underwriting; permissibility varies—confirm current SBA SOP 50 10 8 and lender policy before relying on an earnout. | Recognized structure for SBA buyers when placed on compliant standby with full subordination; does not count toward equity injection. See SBA SOP 50 10 8 landing. |

| Payment Risk (Credit vs. Performance) | Performance risk: KPI may be missed due to market or buyer decisions; strong definitions reduce, but don’t remove, risk. | Credit risk: buyer may default; mitigations include security interests, guarantees, and covenants, subject to subordination/standby. |

| Enforceability & Security Package | Enforcement relies on audit/inspection rights and dispute resolution clauses; hard to secure “performance.” | Clear path to enforce a monetary obligation (UCC filings, guarantees where applicable) though junior to senior/SBA lenders. |

| Tax Timing & Character (U.S.) | Typically eligible for installment reporting of gain under IRC §453; character depends on allocation; avoid service‑like characterization if minimal seller work is intended. | Typically eligible for installment reporting of gain; stated interest is ordinary income to seller and usually deductible to buyer. |

| Complexity & Drafting Burden | High: bespoke KPI definitions, carve‑outs for buyer‑driven changes, accountant‑arbitration ladders. | Lower: standardized note + subordination and, for SBA, a lender‑approved standby agreement. |

| Timeline to Close | Often lengthens negotiations due to KPI modeling and dispute‑mitigation language. | Frequently faster, especially with non‑SBA buyers; for SBA, add underwriting/authorization timeline but drafting is simpler than an earnout. |

| Buyer‑Type Fit | Strategic/PE and flexible family offices often consider it; SBA‑backed buyers may face constraints—confirm with lender. | Strong fit across buyer types; especially practical for SBA‑backed individuals when on compliant standby. |

| Confidentiality & Operational Disruption | Ongoing measurement/audits can increase internal visibility and potential leaks. | Minimal operational intrusion beyond financial reporting for covenants. |

| Typical Terms (as of 2026‑03‑05; market‑dependent) | 1–3 years; capped amounts; objective revenue/EBITDA metrics favored; detailed exclusions for buyer‑driven changes. | 3–5+ year amortization common; subordinated; standby for SBA (no P&I during standby unless lender consents); stated interest at market rates. |

How to choose between earnout vs seller financing by buyer type (California)

SBA‑backed individual buyer

If speed/compliance is the priority and you want minimal post‑close involvement, default to a properly subordinated seller note on lender‑approved standby. SBA policy materials emphasize that equity injection must be true equity and that seller debt is typically treated as subordinated/standby debt—not equity. Classic contingent consideration may complicate repayment analysis, so confirm permissibility with the current SOP 50 10 8 and the specific lender’s policy. For SBA process expectations, many lenders cite roughly 60–90 days from funding application; build that into your timeline.

Strategic or private equity buyer

When there is a real valuation gap but the KPI is truly objective and auditable (e.g., revenue with defined exclusions and audit rights), a narrow, well‑drafted earnout can align incentives without overpaying at close. If your involvement post‑close is limited (0–3 months), favor KPIs that don’t rely on your direct control, or lean back to a fixed seller note for clarity and speed.

Family office or independent sponsor

These buyers often have flexible capital stacks. A hybrid (smaller seller note for certainty plus a capped, conservative earnout for upside) can balance speed to close with incentive alignment. Keep earnout measurement short, objective, and insulated from buyer‑driven changes; secure the note per market norms.

Minimal post‑close involvement (0–3 months)

If you cannot actively influence KPIs after closing, avoid broad earnouts that depend on your hands‑on control. A fixed seller note usually provides a cleaner, lower‑risk path to your proceeds while keeping you out of day‑to‑day operations.

For document expectations and who drafts what, see Business Sale Documents. For diligence readiness that supports lender approval and a smoother close, review Buy‑Side vs Sell‑Side Due Diligence.

SBA and lender compliance in California (what to confirm in 2026)

- SOP reference point: The SBA’s current origination manual is SOP 50 10 8, with ongoing updates. Use the official landing page for the latest edition and confirm change‑of‑ownership sections before locking terms. See the SBA’s page for SOP 50 10 — Lender and Development Company Loan Programs.

- Standby and subordination: SBA workflows recognize seller debt on standby with subordination; lenders often require a standby agreement and entry in ETRAN. See the SBA document index, noting Standby Agreements and lender forms, and the ETRAN guide that references standby entries. Review the SBA’s document index and the ETRAN Loan Authorization Data Entry Guide.

Fun fact (SBA documentation): Even when the economics are straightforward, SBA-backed closings can slow down if the standby/subordination paperwork isn’t perfectly consistent across the note, the standby agreement, and the lender’s internal authorization package—so it’s worth reconciling those documents early.

- Equity injection: Required equity must be true equity; seller financing generally does not count toward the buyer’s equity injection. Confirm with the lender against the current SOP 50 10 8.

- Timelines: Many sources suggest roughly 60–90 days from SBA application to funding, faster with Preferred Lenders and complete packages. See the SBA’s overview of 7(a) loans for program context. Plan diligence to avoid rework that could push closing.

Terms, timing, and tax basics (U.S. federal; 2026)

Think of taxes as another “term” in the deal. Both structures often qualify for installment sale treatment on the gain portion under IRC §453, with interest on a seller note taxed as ordinary income to the seller and typically deductible to the buyer. Sellers report installment gain using Form 6252; see the IRS resource About Form 6252. For current installment rules and special topics (including contingent payments and unstated interest/OID), consult the IRS’s Publication 537 (latest available edition reflected in the IRS listings for 2025, posted Feb. 24, 2026) and Publication 544: IRS Publication 537 (availability/EPUB) and About Publication 544.

Think of taxes as another “term” in the deal. Both structures often qualify for installment sale treatment on the gain portion under IRC §453, with interest on a seller note taxed as ordinary income to the seller and typically deductible to the buyer. Sellers report installment gain using Form 6252; see the IRS resource About Form 6252. For current installment rules and special topics (including contingent payments and unstated interest/OID), consult the IRS’s Publication 537 (latest available edition reflected in the IRS listings for 2025, posted Feb. 24, 2026) and Publication 544: IRS Publication 537 (availability/EPUB) and About Publication 544.

Fun fact (California tax mechanics): If your transaction includes California real estate (e.g., the business owns the building), you may run into California real estate withholding at closing—even if the rest of the deal is a “business sale.” The Franchise Tax Board explains the rules and current forms under FTB Real Estate Withholding.

California overlay: When protecting goodwill, reasonable sale‑of‑business non‑competes are permissible under Business & Professions Code §16601 even though employee non‑competes are broadly void. Law‑firm summaries in 2024–2025 confirm the carve‑out remains intact while general restrictions tightened. See high‑level discussions from Cooley on California non‑competes and Gibson Dunn’s update. Work with counsel to align any earnout or seller‑note covenants with California law.

Rogerson Business Services, California third‑party exits (case studies)

If you're considering an external exit, it's beneficial to check your expectations against recent outcomes. Here are examples of third-party sales from the case-study library (prices, timelines, and challenges vary by industry and company).

- IT services (MSP) — sold for $525K; closed in ~7 months. Case study: How to Sell an IT Services Company in Seven Months.

- Portable sink manufacturer (Bay Area) — closed escrow in ~5 months (third‑party buyer). Case study: Quick Sale of Portable Sink Manufacturer (Bay Area, CA).

- A “failed sale” example (roofing, Northern California) — strong interest, but the process ultimately paused/withdrew. This is useful as a cautionary baseline for pricing and readiness. Case study: The $3 Million Mistake: Why a Northern California Roofing Business Failed to Sell.

For more examples across industries and deal sizes, see the full list: Selling Businesses Case Studies.

Choosing Andrew Rogerson & next steps

You'll need a coordinated deal team, including an M&A advisor or investment banker, tax CPA, transaction attorney (and ERISA counsel for ESOPs), valuation specialists, and, in regulated sectors, licensing experts. Advisors with California closing experience can assist with CDTFA close-outs, bulk sales notices, and landlord or franchisor consents to safeguard price and timing. For details on marketing and process roles, see the internal resources Marketing The Deal and the Deal Team hub.

Advisors who focus on California lower‑middle‑market exits can support valuation, after‑tax modeling, and regulatory navigation (example: Rogerson Business Services). The team is led by Andrew Rogerson (CM&AP), a California M&A advisor with 20+ years in the market—see About for background. Keep the tone of engagement objective and numbers‑driven, and ask for side‑by‑side net‑proceeds models before you commit to a path.

FAQs

Can you use an earnout with an SBA 7(a) loan?

Lenders must follow SOP 50 10 8. Classic contingent consideration can complicate repayment analysis and may be constrained by lender policy. Confirm permissibility with the current SOP and your lender before relying on an earnout. See the SBA’s page for SOP 50 10 — Lender and Development Company Loan Programs.

Which closes faster: an earnout or seller financing?

A plain seller note typically drafts faster than an earnout because it avoids KPI modeling and dispute‑language cycles. SBA‑backed deals often run ~60–90 days from application to funding regardless; plan accordingly using the SBA’s overview of 7(a) loans.

Does seller financing count toward the SBA equity injection?

Generally, no. Seller debt is usually treated as subordinated/standby debt, not equity injection. Confirm with your lender against current SOP 50 10 8 and related documentation workflows such as ETRAN standby entries noted in the ETRAN guide.

How are earnouts and seller notes taxed to the seller?

Both usually qualify for installment sale gain reporting under §453, but note differences: seller‑note interest is ordinary income; earnout character depends on purchase‑price allocation and drafting. See the IRS resource About Form 6252 and Publication 537 (EPUB).

How can sellers reduce litigation risk from an earnout?

Use narrow, objective KPIs; define accounting policies and exclusions for buyer‑driven changes; add audit/inspection rights and a dispute‑resolution ladder (e.g., accountant‑arbitration). Keep the measurement period short and include caps/floors. When in doubt—and if speed is the priority—favor a fixed seller note instead.

Also consider expert help

If you want hands‑on help structuring a California‑compliant deal that prioritizes speed to close and minimal post‑close entanglement, consider a specialized sell‑side advisor such as Rogerson Business Services. The right team can coordinate lender‑compliant seller notes and draft dispute‑resistant earnout terms.

—

This article provides general information and is not legal, tax, or financial advice. Confirm SBA rules, lender policies, and tax treatment with licensed professionals before taking action. As of 2026‑03‑05, ranges and policies may change.

Hey there! Can we send you a gift?

We just wanted to say hi and thanks for stopping by our little corner of the web. :) we'd love to offer you a cup of coffee/tea, but, alas, this is the Internet.

However, we think you'll love our email newsletter about building value and properly position your company before transition/exit your business ownership.

As a special welcome gift for subscribing, you'll also get our helping and educational guides, tips, tutorials, etc.. for free.

It's filled with the best practices for retiring serial business owners like Dan Gilbert, Larry Ellison, Warren Buffett, and many more.

Just sign up for our emails below.