M&A Advisor vs Investment Banker (2026): Which Is Right for a California Owner-Led Exit?

M&A Advisor vs Investment Banker: Pick The Right Advisor

You don’t lose the deal only to valuation. You lose it when you pick the wrong intermediary.

If you run a California owner-led company with $2M–$50M in revenue, the choice between an M&A advisor and an investment banker determines your buyer access, confidentiality posture, timeline, and net after fees.

Here’s the deal: for sub–$50M California exits that prize discretion and hands-on guidance, a specialized M&A advisor usually fits best; for scaled, complex, or $50M+ transactions, an investment bank’s broad auction and capital markets reach can win.

Guide Context

For context on who this guide is written for: Rogerson Business Services’ ideal client is a California business owner planning an exit or sale, typically with $2 million to $50 million in annual revenue, in industries such as manufacturing, construction, managed IT, business services, industrial services, industrial products, healthcare, logistics and transportation, and wholesale distribution.

This guide is also informed by the perspective of Andrew Rogerson—a California M&A advisor with 20+ years in the market and credentials including Certified Mergers & Acquisition Professional (CM&AP)—see the firm’s About page.

Let’s dig in.

Key takeaways

- For a $25M revenue / $4M EBITDA California industrial services company targeting a 9–12 month close with strict confidentiality, an experienced M&A advisor is the better default fit.

- Choose an investment banker when enterprise value approaches or exceeds ~$50M, you need a broad, multi-round auction, or the deal spans multi-state/regulatory complexity.

- Use a size/complexity/control decision framework and factor the federal 2023 M&A broker exemption alongside California privacy (CCPA/CPRA), CDTFA/FTB clearances, and escrow practices.

TL;DR: The anchor scenario verdict

For our anchor profile—a $25M revenue / $4M EBITDA California industrial services company that needs a confidential process and a 9–12 month close—pick an M&A advisor. A targeted process with staged NDAs, minimal-disclosure marketing, and California-specific diligence controls keeps identity protected and buyer focus sharp.

If your facts shift to ≥$50M EV, multi-state healthcare, or you want a broad PE/strategic auction, shift to an investment banker. That’s the core decision framework: size/complexity and confidentiality/control decide the winner.

Next step (sell-side readiness): Use the Sell-Side Due Diligence Checklist to organize diligence materials early, reduce re-trades, and run a cleaner process—especially in California.

Side-by-side snapshot: M&A advisor vs investment banker

Below, we present concise fields that owners actually use to decide. We order rows by scenario relevance for California lower middle market sellers.

| Role | Typical EV fit | Buyer universe | Process style | Confidentiality controls | Fee model & typical ranges (as of 2026-03-07) | Typical timeline | Diligence/QoE support | CA regulatory strengths | Best for | Evidence/source |

|---|---|---|---|---|---|---|---|---|---|---|

| M&A Advisor | Sub-~$50M owner-led California deals | Strategics, select PE/family offices, niche buyers | Targeted, discreet outreach | Blind teaser, staged NDAs, CCPA/CPRA-aligned data room | Retainer + tiered success fees (Lehman variants) with flexibility | ~6–9 months prep to close in many LMM cases | Coordinates sell-side QoE and organized data room | Streamlines CDTFA/FTB clearances and escrow norms | Confidential, hands-on exits under ~$50M | Wall Street Prep on timelines; Axial fee guides; CPPA/AG; CDTFA/FTB |

| Investment Banker | ~$50M+ or complex, multi-state/regulatory | Broad strategics, PE platforms, cross-border pools | Broad, multi-round auction cadence | Standard NDAs, broader teaser/CIM circulation | Larger retainers/minimums; lower % on higher EV | ~6–10+ months for scaled auctions | Larger teams standardize rigorous auction diligence | Strong at complex financing and R&W usage | Maximizing competition on larger/complex deals | M&I/WSP primers; Axial/PwC market context |

Caption: Timelines reflect common sell-side benchmarks from the sell-side process overviews by Wall Street Prep and market practice. Fee range framing follows Axial’s 2023–2025 fee guides. California privacy controls reference the CPPA/AG guidance, while state close mechanics reference CDTFA/FTB resources. Links appear once each below.

Method note (how to read the ranges): The ~$50M breakpoint, fee structures, and timeline ranges in this table reflect common market patterns described in third-party sell-side process and fee references (for example, Wall Street Prep on process timing and Axial on advisory fee structures), plus practical California closing mechanics from primary state sources (for example, CDTFA and FTB guidance). Treat the cutoffs as directional, not hard rules—industry, buyer type, readiness, and deal structure can move the “right fit” line up or down.

Don't have time to read more?

Take a shortcut and play the video overview below

Walk through the anchor case: how the process actually runs

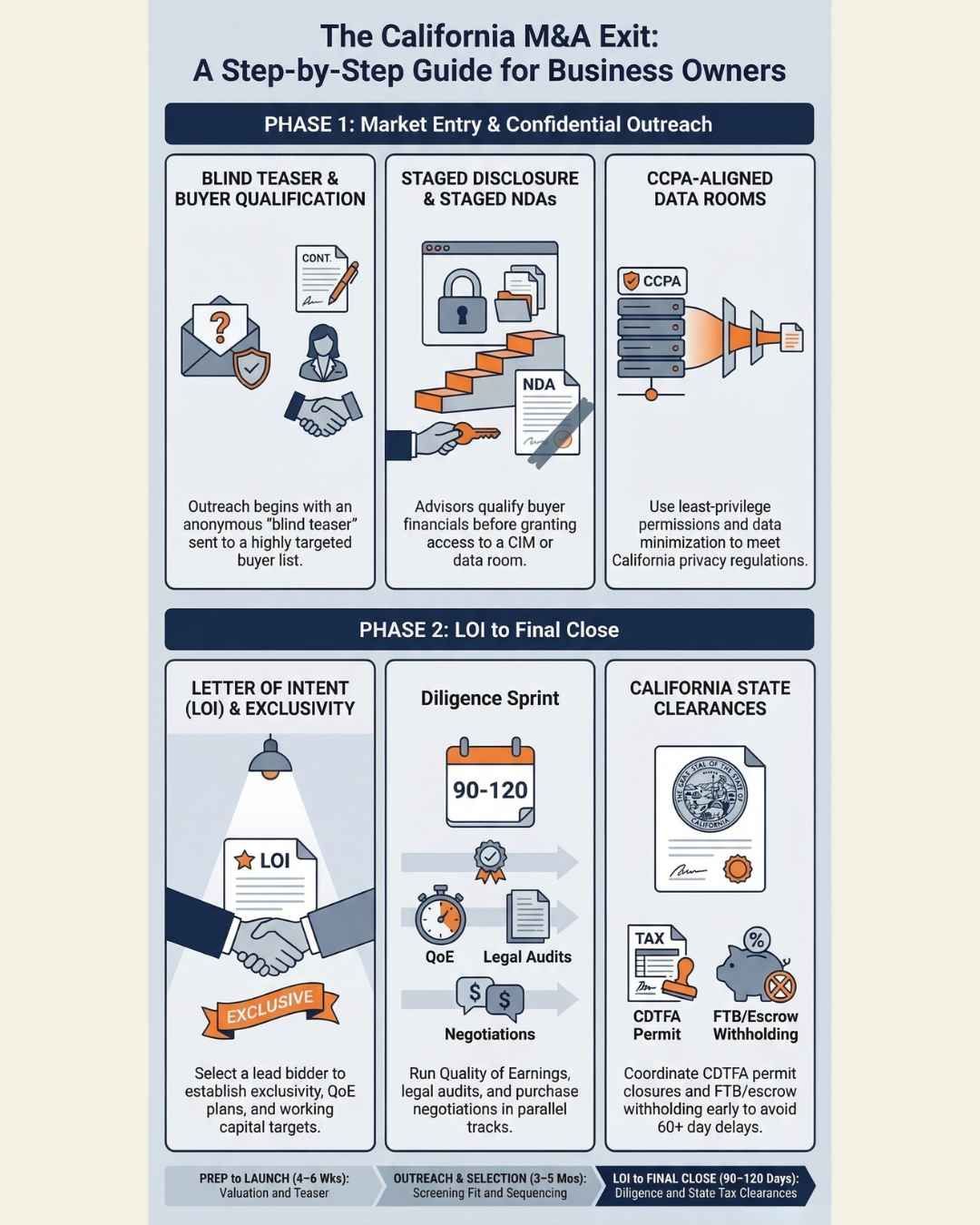

Start with a blind teaser and a tight buyer list. Your advisor qualifies interest and financial capability before any NDA. After you countersign a tailored NDA, your advisor stages access: a concise CIM, then a controlled data room with least-privilege permissions. They time disclosures to key milestones and minimize personally identifiable information to align with California privacy rules. According to California regulators (CPPA/AG), diligence disclosure can qualify as a “business purpose” if contracts impose equivalent protections and you honor prior opt-outs after closing; that’s why staged NDAs and data minimization matter.

Next, your advisor sets the cadence. They schedule initial conversations, screen cultural fit, and sequence a small set of high-probability strategics and family offices. You keep the circle tight to protect employees and customers from premature leaks. Once you select a leading bidder, you push to an LOI with clear exclusivity, a QoE plan, and working capital targets. From LOI, you often drive to close in ~90–120 days with QoE, legal diligence, and purchase agreement negotiations running in parallel. In California, your advisor also coordinates CDTFA seller-permit closure and FTB/escrow steps early to reduce the risk of last-minute surprises.

Could an investment banker improve this outcome? If your priority shifts to the broadest competition—say you want two auction rounds with a wide PE pool—yes. But for the $25M/$4M industrial services profile, you usually gain more by staying discreet, managing confidentiality, and targeting the buyers who truly pay for fit.

California outcome example

A real California outcome example (anonymized): In one California manufacturing engagement, the seller closed at $36M after running a broad initial buyer screen and contacting 89 potential buyers. That’s the practical trade-off: you can expand the top of the funnel while still controlling identity disclosure through a blind teaser and staged NDA process—especially when you work backward from your confidentiality risk (employees, customers, competitors) instead of defaulting to the widest possible auction. Learn more about this deal.

A second California mini-snapshot (different size/industry): In a Sacramento-based IT managed services engagement, the seller closed a deal for an IT services business valued at $525K in about seven months (launch in July 2022; close on January 13, 2023). The company ran a break-fix model serving small-to-mid-sized businesses, and the seller strengthened the books before launch by upgrading bookkeeping and financial statements—then kept the process moving with disciplined buyer qualification so momentum didn’t drift. Learn more about this deal.

How to choose in California: M&A advisor vs investment banker

Use this simple, practical flow.

- If enterprise value is below ~$50M in California and you rank confidentiality and owner control as top priorities, choose an M&A advisor to run a targeted process and align with CCPA/CPRA and state close mechanics.

- If enterprise value is ≥$50M, the deal spans multiple states or complex payor/regulatory regimes, or you want a broad PE/strategic auction, choose an investment banker for scale, multi-round process discipline, and financing orchestration.

- If you need to close in under six months and you already know likely strategic buyers, consider a highly targeted advisor-led outreach rather than a full auction.

- If QoE risk runs high due to customer concentration or messy books, engage an M&A advisor with a robust sell-side readiness program or pause to remediate first.

About licensing: In 2023, Congress codified a federal M&A broker exemption in Exchange Act §15(b)(13), effective March 29, 2023, which replaced the 2014 no-action letter. Analyses by Mayer Brown and K&L Gates explain the scope and limitations.

The exemption clarifies certain activities for private company deals, yet you still must consider state-level requirements and what activities your intermediary performs. Use it as context, not as a substitute for legal advice.

Fees, timelines, and net-after-fee math (as of 2026-03-07)

Timelines: Many lower middle market sell-side processes span ~6–9 months from preparation through close, with roughly 4–6 weeks per phase and ~90–120 days post-LOI to finalize diligence and definitive agreements, per established process references.

Fees: In the Lower Middle Market (LMM), advisors commonly charge a retainer plus tiered success fees (Lehman variants) that step down with larger sizes. Investment banks often quote lower percentage success fees at higher absolute dollars and may require larger retainers or minimums. Ranges vary by complexity and competition. Always evaluate net after fees and taxes rather than the headline price.

Illustrative net-after-fee sensitivity (for simple comparison only):

| Sale price | Success fee 8% | Success fee 6% | Success fee 3% |

|---|---|---|---|

| $20,000,000 | $18,400,000 | $18,800,000 | $19,400,000 |

| $30,000,000 | $27,600,000 | $28,200,000 | $29,100,000 |

Note: This excludes retainers, expenses, taxes, working capital adjustments, and R&W premiums; use it to frame directionally how fee percentages affect proceeds.

How to choose: M&A advisor vs investment banker in California (decision framework)

Make confidentiality a system, not a promise. Run teaser → NDA → CIM → data room with clear access logs and least-privilege permissions.

Align diligence with CCPA/CPRA obligations by contract and by design. For state close mechanics, coordinate CDTFA seller-permit closure and FTB escrow/withholding early—escrow officers may hold funds if liabilities appear, and clearances can take 60+ days depending on the facts and agency timing.

For a practical walkthrough of the sequence and owner responsibilities, see the sell-side overview in the Rogerson resource Walk Me Through A Sell Side M&A Deal. For documents you should prepare up front, use the Sell-Side Due Diligence Checklist.

If you want a plain-English refresher on role definitions while you evaluate advisors, readM&A Advisors vs. Investment Bankers | Which One To Pick.

FAQs

Which is better for selling a $25M California business—an M&A advisor or an investment banker?

For a $25M revenue / $4M EBITDA owner-led business prioritizing confidentiality and a 9–12 month close, an experienced M&A advisor typically fits best. If your needs shift to a broad auction or ≥$50M EV, an investment banker’s scale can help. Timeline and auction cadence benchmarks come from established sell-side process overviews.

What does the 2023 M&A broker exemption mean for California sellers?

Exchange Act §15(b)(13) (effective March 29, 2023) codified a federal exemption for certain M&A broker activities and withdrew the 2014 no-action letter, as leading law firm analyses confirm. It clarifies federal treatment but does not eliminate state considerations or sector-specific nuances—discuss scope with counsel.

How much do M&A advisors charge vs investment bankers?

Advisors commonly use a retainer plus tiered success fees (Lehman variants) in the lower middle market. Banks often quote lower percentages but higher retainers or minimums at larger EVs. Industry guides document current norms; your exact fee depends on size, complexity, and competition for the mandate.

How can I protect confidentiality when selling my California business?

Use blind teasers, staged NDAs, minimal-disclosure CIMs, and a vendor-controlled data room with logging. Ensure your contracts and access controls align with CCPA/CPRA expectations so diligence sharing qualifies as a business purpose, and honor prior opt-outs post-close, per California privacy regulators.

When should I hire an investment bank instead of an M&A advisor?

Choose a bank when EV is ≥$50M, you need a wide PE/strategic auction with multi-round bidding, you face complex multi-state or regulated dynamics, or you need financing orchestration and large-team diligence.

Sources and further reading

- Federal 2023 M&A broker exemption overviews: see Mayer Brown’s analysis in “New federal exemption from broker registration… effective on March 29, 2023 (Prior SEC No-Action Relief Has Been Withdrawn)” and K&L Gates’ summary of scope and limits.

- California privacy regulators: review the CPPA/AG CCPA hub and final regulations text for diligence-sharing and contract requirements.

- Sell-side process timing: consult Wall Street Prep’s sell-side process overview for phase lengths and LOI-to-close timing.

- Fee norms and advisor economics: examine Axial’s 2023–2025 M&A fee guides for market-typical structures and commentary.

- California tax/escrow mechanics: see CDTFA Publication 74 on closing out permits and the FTB bulk sale/withholding guidance for escrow coordination.

External links (one per source):

- Mayer Brown on §15(b)(13):https://www.mayerbrown.com/en/insights/publications/2023/04/new-federal-exemption-from-broker-registration-for-ma-brokers-became-effective-on-march-29-2023-prior-sec-no-action-relief-has-been-withdrawn

- K&L Gates analysis:https://www.klgates.com/United-States-Goodbye-MA-Brokers-No-Action-Letter-Hello-Federal-Exemption-3-30-2023

- CPPA/AG CCPA hub:https://oag.ca.gov/privacy/ccpa

- Wall Street Prep sell-side overview:https://www.wallstreetprep.com/knowledge/sell-side-process/

- Axial fee guide index:https://www.axial.net/forum/ma-fee-guide-2023-2024/

- CDTFA Publication 74:https://cdtfa.ca.gov/formspubs/pub74.pdf

- FTB bulk sale certificate:https://www.ftb.ca.gov/help/business/bulk-sale-certificate.html

Internal Rogerson resources (helpful, non-promotional)

- Walk Me Through A Sell Side M&A Deal:https://www.midmarketbusinesses.com/mergers-acquisitions-advisory/walk-me-through-a-sell-side-m-a-deal

- Sell-Side Due Diligence Checklist:https://www.midmarketbusinesses.com/business-owners/sell-side-due-diligence-checklist

- M&A Advisors vs. Investment Bankers | Which One To Pick:https://www.midmarketbusinesses.com/ma-concept-comparison/ma-advisors-vs-investment-bankers

Author’s note on practical experience

Andrew Rogerson, founder of Rogerson Business Services, is a 5-time business owner and author of four books. He holds credentials including CBB, CM&AP, and M&AMI, and applies a confidentiality-first approach common to California lower middle market sell-side engagements. Optional credential references: Clarity.fm profile, CABB broker directory listing, and a YouTube interview. Use this framework and the cited sources to map your facts, then select the intermediary that best fits your size, complexity, and control priorities.

Hey there! Can we send you a gift?

We just wanted to say hi and thanks for stopping by our little corner of the web. :) we'd love to offer you a cup of coffee/tea, but, alas, this is the Internet.

However, we think you'll love our email newsletter about building value and properly position your company before transition/exit your business ownership.

As a special welcome gift for subscribing, you'll also get our helping and educational guides, tips, tutorials, etc.. for free.

It's filled with the best practices for retiring serial business owners like Dan Gilbert, Larry Ellison, Warren Buffett, and many more.

Just sign up for our emails below.