Asset Sale vs Stock Sale (2026): Why Deal Structure Beats Offer Price in California

Asset Sale vs Stock Sale: Deal Structure And Offer Price

By Andrew Rogerson, CM&AP, LCBB (Rogerson Business Services).

Andrew Rogerson is an M&A advisor and a 35+ year business owner who helps California lower and mid-market owners value, position, and sell their companies through sell-side representation—credentials: CM&AP and LCBB listing.

A buyer can offer you the same headline price under two different structures, and you can still walk away with very different money in your pocket. This guide compares an asset sale vs stock sale for California owners and shows why the deal structure, not the offer price, ultimately determines your net after-tax proceeds, your risk, and your path to a clean close.

TL;DR verdict: Structure > price. In California, tax character, purchase price allocation (Form 8594), potential sales tax on assets, and elections like §338(h)(10)/§336(e) can swing seller net proceeds by six figures on the same headline price.

Note on scope: Tax and legal facts are as of 2026-03-07 and may change. Use this article for education only.

Guide Context

For context on who this guide is written for: Rogerson Business Services’ ideal client is a California business owner planning an exit or sale, typically with $2 million to $50 million in annual revenue, in industries such as manufacturing, construction, managed IT services, industrial services, business services, healthcare, logistics and transportation, and wholesale distribution.

The topic: Asset Sale vs. Stock Sale is also informed by the perspective of Andrew Rogerson, a California M&A advisor with 20+ years in the market and credentials including Certified Mergers & Acquisition Professional (CM&AP)—see the firm’s About page.

Let’s dig in.

Key takeaways

- The winner is the structure that maximizes your net after-tax proceeds for your facts. The same price can yield very different checks at closing.

- California taxes capital gains at ordinary income rates—no lower long-term rate—so character and allocation matter even more than in other states.

- Asset deals can trigger California sales tax on fixtures/equipment/inventory and ordinary income recapture; stock deals often avoid those but may transfer more liabilities.

- Elections (§338(h)(10)/§336(e)) can bridge the gap: buyers get a basis step-up while sellers negotiate a price gross-up to protect net.

- Documentation drives outcomes. Form 8594 allocations, clean QoE, and license/contract paths reduce retrades and speed closing.

Asset Sale vs Stock Sale at a glance (with §338(h)(10)/§336(e))

Before we dive into the math, here’s a side‑by‑side look at the key differences that drive results for California sellers.

| Dimension | Asset sale | Stock sale | With §338(h)(10)/§336(e) election |

|---|---|---|---|

| Headline price | Same starting point for comparison | Same | Same |

| Net after-tax proceeds potential | Can be lower for sellers due to ordinary income recapture and possible CA sales tax | Often higher for sellers (generally capital gain) | Can approximate asset economics for buyer with negotiated seller protection |

| Tax character of gain | Mix of capital gain and ordinary income (recapture; inventory/AR at ordinary) | Generally capital gain to the selling shareholder | Deemed asset sale at target; recapture may apply; priced with seller gross‑up |

| Purchase price allocation | Required via Form 8594; allocation across Classes I–VII drives tax character | No Form 8594 filing (absent election) | Allocation reported on Form 8883 (deemed asset sale) |

| Buyer basis step‑up | Yes; enables depreciation/amortization (incl. §197 intangibles) | No step‑up (stays at historical basis) | Yes; deemed step‑up via election |

| Successor liability | Typically limited to selected liabilities, but exceptions exist | Buyer inherits target’s liabilities | Same as stock for legal form; tax treatment like asset |

| License/contract friction (CA) | Assignments/approvals may delay close in regulated sectors | Often smoother continuity (entity unchanged) | Same operationally as stock; tax like asset |

| Closing speed/certainty | Can slow due to assignments, allocations, and sales tax steps | Often faster in licensed industries; diligence still key | Similar to stock; add election filings and tax modeling |

| Escrow/holdback patterns | Often used to cover tax/indemnity exposure | Often used to cover broader successor risks | Similar to stock; sometimes smaller with RWI |

| Ideal seller profile | Owners prioritizing buyer premium or asset‑heavy buyers that demand step‑up | Retiring owners seeking higher net and simpler tax | S‑corp/LLC sellers where buyer needs step‑up and seller can be made whole |

Footnote: Definitions and fundamentals are explained in the Rogerson Business Services overview on asset sale vs. stock sale. For allocations, see the IRS guidance on Form 8594 and the residual method.

Don't have time to read more?

Take a shortcut and play the video overview below

Why structure—not headline price—drives your net after-tax proceeds

- California treats long‑term and short‑term capital gains the same; there’s no preferential long‑term rate. That makes the character of your gain and your purchase price allocation even more important. See the Franchise Tax Board’s guidance on

capital gains and losses in California.

Strategic bite: If you’re comparing two LOIs at the same price, don’t start with the purchase price. Start with a one‑page “seller net bridge” that shows (1) taxes by bucket, (2) transaction costs, (3) escrow/holdback, and (4) working capital adjustment. That bridge usually reveals which deal actually pays you more. - Asset sales often recharacterize part of the deal as ordinary income. Depreciation recapture on equipment and certain real property, plus inventory and accounts receivable, can be taxed at ordinary rates, lifting your bill relative to a stock sale. The IRS explains recapture mechanics in

Publication 544 (Sales and Other Dispositions).

Concrete micro‑example: When the buyer allocates more value to equipment (because they want faster depreciation), you may pay more tax at ordinary rates on recapture. That means a “better” allocation for the buyer can be a worse allocation for you—unless you negotiate a price adjustment. - The 3.8% Net Investment Income Tax can apply to passive owners’ gains. Whether it applies depends on your activity level and entity facts; review the IRS’s

Net Investment Income Tax overview.

Pro tip: Ask your CPA to run NIIT both ways—“active” and “passive”—before you sign the LOI. If you get surprised late, you lose leverage to fix the price or structure. - California sales/use tax can reduce your net in asset deals when fixtures, equipment, or inventory change hands unless an exemption applies (for example, some occasional sales scenarios). The California Department of Tax and Fee Administration outlines seller obligations in

Publication 74: Closing Out Your Account.

Strategic bite: Sales tax doesn’t feel like “deal structure,” but it behaves like one because it can come straight off the top of your proceeds. If tangible assets matter in your business (fleet, machinery, shop equipment, inventory), treat “sales tax outcome” as a line item in your net proceeds model—not a footnote. - Real property held in entities can be reassessed when control or ownership changes under California’s property tax rules (RTC §64). The Board of Equalization describes triggers and filings in its

Property Tax overview.

Concrete micro‑example: If your company owns the building and the deal changes control, a property tax reassessment can raise the ongoing tax bill. Even if the buyer pays it after closing, they may push back on price or terms once they model it.

Deal-term bites that often move net proceeds (even when price stays flat)

- Working capital peg: Buyers often propose a “normalized working capital” target. If it’s too high, you effectively fund the buyer at close through a purchase price reduction.

- Escrow/holdback: A larger escrow doesn’t always mean more risk; sometimes it means the buyer didn’t get comfortable with diligence. You can trade escrow size for clearer reps, narrower indemnities, or reps & warranties insurance.

- Allocation language in the LOI: If the LOI says “allocation to be determined later,” you invite a late fight that you usually lose. Align early on principles (for example, independent valuation for key asset classes), so the Form 8594 work doesn’t become a retrade.

Think of structure as the blueprint that defines which tax rules apply to each dollar and which filings you must make. Price sits on top of that blueprint; it doesn’t rewrite it.

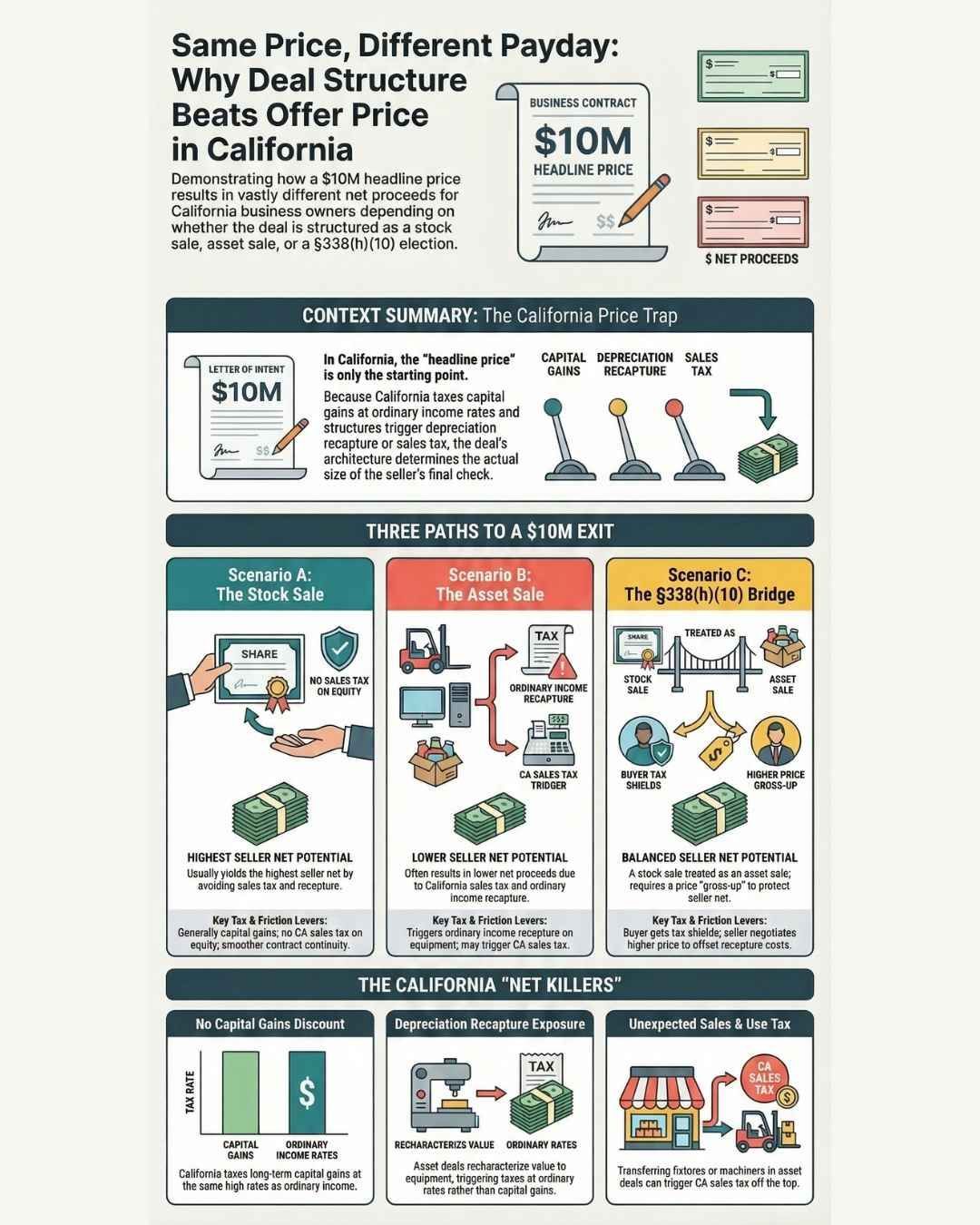

A simple California mini‑case: same price, different cash in your pocket

Assumptions & limitations (read this first): This mini‑case is illustrative, not a quote or a tax calculation for your situation.

- Entity & owner status: Assumes an S‑corp with an active owner. If you’re a C‑corp, have multiple owners, or are passive, the answer can change.

- NIIT: We assume NIIT may not apply because the owner is active, but your CPA should test both outcomes (active vs. passive).

- Sales tax: We assume California sales tax may apply to taxable tangible assets in an asset deal, and we do not assume an exemption.

- Allocation drives the result: Small shifts in purchase price allocation (Form 8594 / Form 8883) can materially change ordinary income vs. capital gain.

- Deal terms change your check: Working capital adjustments, escrows/holdbacks, and fees can change “net at close” even when the headline price stays the same.

Use this example to spot the levers, then ask your CPA/tax attorney to model your numbers before you sign an LOI.

Assumptions (illustrative only)

- Headline price: $10,000,000; Selling shareholder owns 100% and plans to retire in California.

- Seller basis by class: low basis in equipment; moderate basis in goodwill; minimal AR/inventory retained by buyer in stock scenario.

- Entity: S‑corp with active owner; NIIT may not apply; assume typical transaction costs and a modest escrow.

- California: no preferential long‑term capital gains rate; sales tax may apply to fixtures/equipment in an asset deal; no exemption assumed here.

Scenarios

- Stock sale (no election): Most of the gain is capital in nature. No California sales tax on the equity transfer. Buyer does not receive a basis step‑up. Result: higher seller net, but buyer loses tax shields and may offer a lower price without an adjustment.

- Asset sale: Allocation on Form 8594 pushes value into equipment (recapture at ordinary rates) and goodwill (§197 intangibles). California sales tax applies to taxable tangible assets, reducing the seller's net. Result: lower seller net unless the buyer pays a premium.

- Stock sale with §338(h)(10): Parties elect to treat it as a deemed asset sale for tax; buyer gets a basis step‑up and can amortize intangibles. Seller faces recapture like an asset sale, so negotiates a price gross‑up to keep net competitive with the straight stock sale.

Result: balanced economics if priced correctly.

These are directional outcomes. Your actual numbers depend on your entity type, basis, allocation, buyer’s needs, and California‑specific taxes.

For context on allocations, see the IRS guidance on Form 8594 and, for deemed asset sales, Form 8883 (Section 338).

For a primer on California capital gains in business sales, see Rogerson Business Services (RBS’s) explainer on how California taxes capital gains when you sell a business.

For the asset‑deal sales tax context, see Rogerson Business Services' (RBS’s) guide to who pays sales tax on an asset sale in California.

How to choose: fast decision tree and a 10‑point checklist

A quick way to think about it.

- If you want the highest seller net and your buyer can live without a step‑up, push for a stock sale.

- If your buyer needs a step‑up to make the deal pencil, explore a §338(h)(10) or §336(e) path with a price gross‑up.

- If your company is asset‑heavy and sales tax would bite, weigh a stock sale unless an exemption clearly applies.

- If licenses or contracts are hard to transfer quickly, stock can speed closing by preserving continuity.

10‑point checklist

- Define your priority: net after‑tax proceeds, closing speed, or liability profile.

- Map your basis by asset class; estimate recapture exposure.

- Model California income tax on gain and check NIIT applicability.

- Confirm if California sales/use tax would apply in an asset deal.

- Identify license and contract transfer hurdles in your industry.

- Pressure‑test buyer pricing under each structure (step‑up vs no step‑up).

- Consider §338(h)(10)/§336(e) eligibility and fit for your entity and buyer.

- Align on allocation methodology (Form 8594 or Form 8883) early in LOI.

- Right‑size escrow/indemnity terms and evaluate RWI to protect your net.

- Build a signed‑to‑close calendar for approvals, filings, and elections.

Elections that bridge the gap: Section 338(h)(10) and 336(e)

These elections let parties treat a stock transfer as a deemed asset sale for tax purposes when eligibility requirements are met. Buyers usually want the resulting basis step‑up; sellers need price protection because recapture and other asset‑sale tax effects can increase their bill.

Strategic bite: Treat an election like a “trade”: you give the buyer tax shields, and you ask for seller‑net protection in return. If you wait to discuss that trade until after diligence, you usually negotiate from a weaker position.

- §338(h)(10): Requires a qualified stock purchase (generally 80% or more of the vote and value within 12 months) and a joint election; file on the IRS’s

Form 8023 by its deadline. Allocation in the deemed asset sale is reported on

Form 8883.

Pro tip: If a buyer hints at a §338(h)(10) election, ask this early: “Will you pay for the election economics?” In plain English, that means you model the deemed asset sale tax and then negotiate a purchase price gross‑up (or other value) so your net stays competitive with a straight stock sale. - §336(e): Can allow seller‑side elections in certain S‑corp and consolidated settings without buyer consent. A practical overview is available from

Pillsbury’s explainer

on

the 338(h)(10)/336(e) election landscape.

Concrete micro‑example: You can structure the legal deal as a stock sale (which can keep contracts and licenses in place) but still create asset‑sale tax results. That combination often makes the election a useful “middle option” when the buyer wants a step‑up, but you want operational continuity.

Common seller traps to avoid

- You agree to the election in concept, but you don’t price it. If you sign an LOI that says “seller will cooperate with a 338 election” and nothing else, you may absorb the tax cost.

- You don’t set a modeling deadline. Put a timeline on it: “We will finalize structure and election intent before definitive docs,” so it can’t become a last‑minute retrade.

- You ignore purchase price allocation until the end. Elections still require allocations (Form 8883). Allocation fights often hide inside “tax language,” but they change your check.

Deal-term bite: If the buyer insists on election economics, you can sometimes trade it for tighter deal terms—such as a smaller escrow, a lower indemnity cap, or a shorter survival period—because the buyer already “gets paid” through the tax step‑up.

Price, timing, and eligibility determine whether an election actually helps. Coordinate your CPA, tax attorney, and M&A advisor early so the LOI reflects the chosen path.

About Rogerson Business Services: Rogerson Business Services is a California-based sell-side M&A advisory firm focused on lower middle-market businesses (roughly $2M–$50M in annual revenue). The deal team has advised California owners for 20+ years and across 100+ transactions, including businesses in manufacturing, distribution, B2B services, industrial services, healthcare, and logistics/trucking. See some of the successful war stories from the trenches.

California licensing and contracts: where friction can flip your choice

In regulated sectors, the smoother path to keep revenue flowing can become the tiebreaker.

Strategic bite: Don’t treat licensing as “post‑close cleanup.” Treat it like a gating item that can delay closing, trigger a purchase price adjustment, or force an unwanted structure.

What to ask early (plain-English, LOI stage):

- “Which licenses, permits, and customer contracts require consent or a new application if we do an asset deal?”

- “If we do a stock deal, which regulators still require notice or approval?”

- “What’s the realistic approval timeline, and what is the drop‑dead date (outside date) if approvals drag?”

- Healthcare facilities: Many licenses are not transferable; changes of ownership or stock transfers require prior approval. The Department of Public Health outlines processes in its

CHOW/stock transfer packets.

Pro tip: Build licensing into the purchase agreement as a condition to close, and match it with a clear outside date. If approval slips, you want a clean decision point instead of an open‑ended “we’ll see.” - Contractors: Licenses tied to the business entity and qualifier; asset sales may require new licensing, while stock can preserve continuity with filings. See the Contractors State License Board’s guidance to

maintain and change your license.

Concrete micro‑example: If the business depends on a qualifier, the buyer may ask for a longer transition, a consulting agreement, or a holdback tied to license continuity. Those terms can matter as much as taxes. - Trucking/logistics: Authority and registrations (FMCSA/USDOT, DMV occupational licenses) must be updated or reissued; stock deals can reduce downtime if handled correctly. Review the FMCSA’s guidance on

updating your registration.

Deal-term bite: If authority or registrations could lapse, buyers often push for (1) an escrow for claims that arise during the transition or (2) a purchase price adjustment if revenue drops. You can reduce that pressure by building a detailed signed‑to‑close transition plan (who files what, by when, and what evidence the buyer needs).

When licenses are hard to transfer, a stock sale often wins on speed and certainty—even if the buyer prefers asset economics—because continuity can be priceless.

FAQ: quick answers for California owners

Which is better for California business owners: an asset sale or a stock sale?

It depends on priorities. Sellers often net more under a stock sale because gains are generally capital in nature, and California equity transfers avoid sales tax. Buyers prefer asset economics for the basis step‑up. Elections can balance both.

How does a §338(h)(10) election affect seller net proceeds in California?

It makes a stock sale a deemed asset sale for tax, giving buyers a step‑up but exposing the seller to recapture and other asset‑sale effects. Sellers usually seek a price gross‑up. See the IRS process on Form 8023.

Will I pay California sales tax if I sell my company’s assets?

Possibly. Sales of fixtures, equipment, and inventory in an asset sale can be taxable unless an exemption applies. Review CDTFA’s seller guidance in Publication 74 and get advisor confirmation.

How do I use Form 8594 to allocate purchase price after a business sale?

In applicable asset acquisitions, the buyer and seller file Form 8594 using the residual method to assign price across Classes I–VII. Allocation controls tax character and audit resilience. See the IRS page on Form 8594.

Why does California’s capital gains rule matter so much here?

Because California doesn’t offer a lower long‑term capital gains rate, shifting dollars from ordinary income to capital gain (and avoiding sales tax where possible) can significantly change your net. See the FTB’s page on capital gains and losses.

Resources and expert help

Authoritative references

- IRS —Publication 544: Sales and Other Dispositions (2026 online edition)

- IRS —About Form 8594 (Asset Acquisition Statement)

- IRS —About Form 8883 (Asset Allocation Statement under Section 338)

- Franchise Tax Board —Capital gains and losses in California

- CDTFA —Publication 74: Closing Out Your Account

- California BOE —Property Tax overview (RTC §64 context)

More California‑specific reading from Rogerson Business Services

- RBS —Asset sale vs. stock sale: California Explainer

- RBS —How California Taxes Capital Gains When Selling a Business

- RBS —Who Pays Sales Tax on an Asset Sale of a Business in California

Also consider

- If you want a California‑specific proceeds model and election analysis, Rogerson Business Services is particularly strong in modeling after‑tax outcomes and evaluating §338(h)(10)/§336(e) options for lower middle‑market sellers. Learn more at Rogerson Business Services.

Disclaimer

- This article provides general information and is not tax, legal, or accounting advice. Facts and law are as of 2026‑03‑07 and may change. Consult a CPA and tax attorney before you sign an LOI or make an election.

Hey there! Can we send you a gift?

We just wanted to say hi and thanks for stopping by our little corner of the web. :) we'd love to offer you a cup of coffee/tea, but, alas, this is the Internet.

However, we think you'll love our email newsletter about building value and properly position your company before transition/exit your business ownership.

As a special welcome gift for subscribing, you'll also get our helping and educational guides, tips, tutorials, etc.. for free.

It's filled with the best practices for retiring serial business owners like Dan Gilbert, Larry Ellison, Warren Buffett, and many more.

Just sign up for our emails below.