Asset Sale vs Stock Sale:

The Ultimate Comparison

Navigating the strategic decision between an asset and stock business sale in California. Understand how deal structure affects tax liabilities, basis step-up, and legal risk with Andrew Rogerson, M&A Advisor, founder of Rogerson Business Services, helping business owners exit their business ownership with deals valued from $2 to $100 million.

License & CredentialS

CA BRE# 01861204

M&AMI

Master Intermediary

LCBB

Lifetime Broker

CM&AP

M&A Professional

CABB

CA Assoc. Bus. Brokers

M&A Source

Global Association

Comparison Matrix: Asset vs. Stock Sale

Detailed breakdown of operational and financial differences.

| Category | Asset Sale Structure | Stock Sale Structure |

|---|---|---|

| (Legal) Entity Status | Remains with Seller (shell) | Transfers to Buyer (intact) |

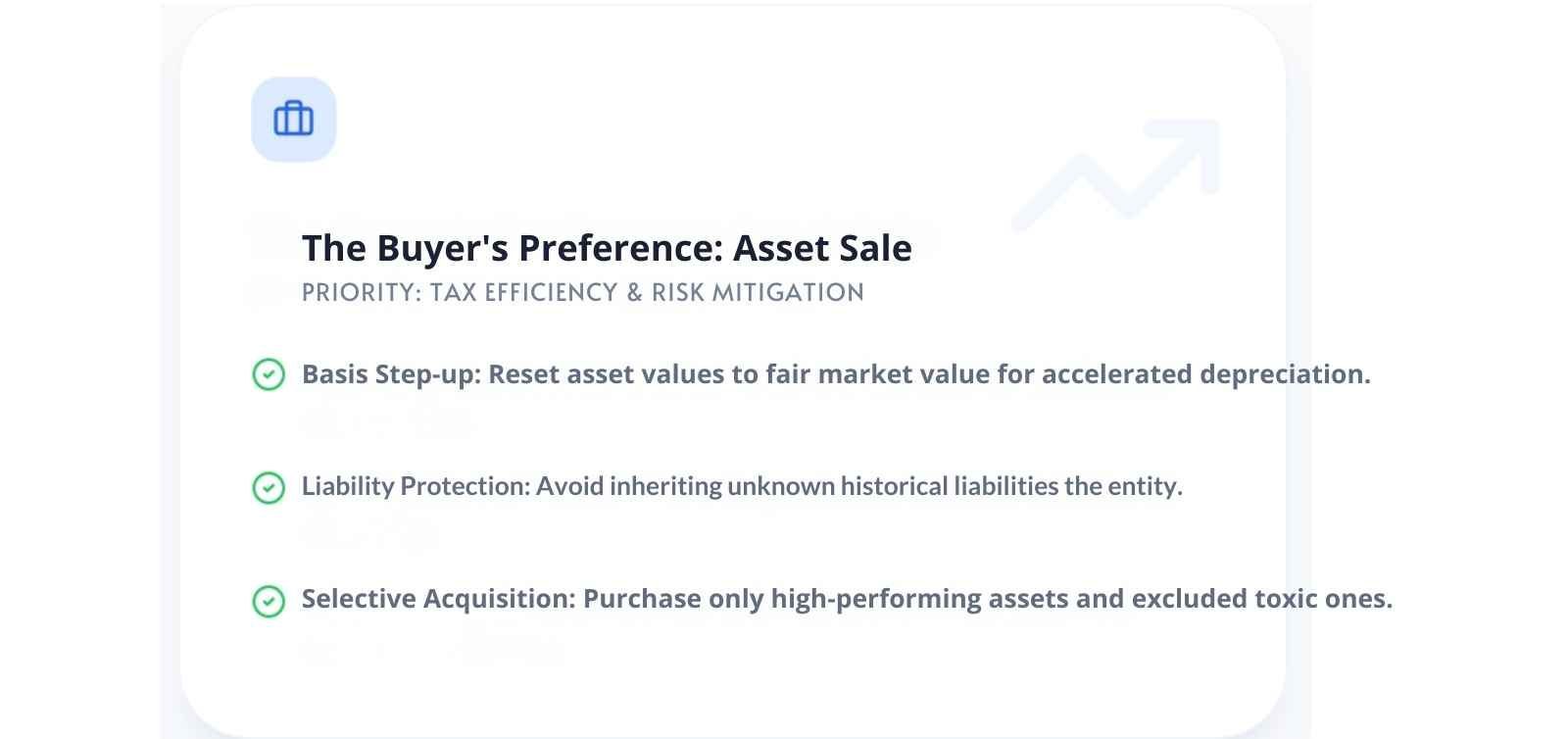

| (Taxation) Tax Treatment (Buyer) | Basis "Step-up" to FMV | Carryover basis |

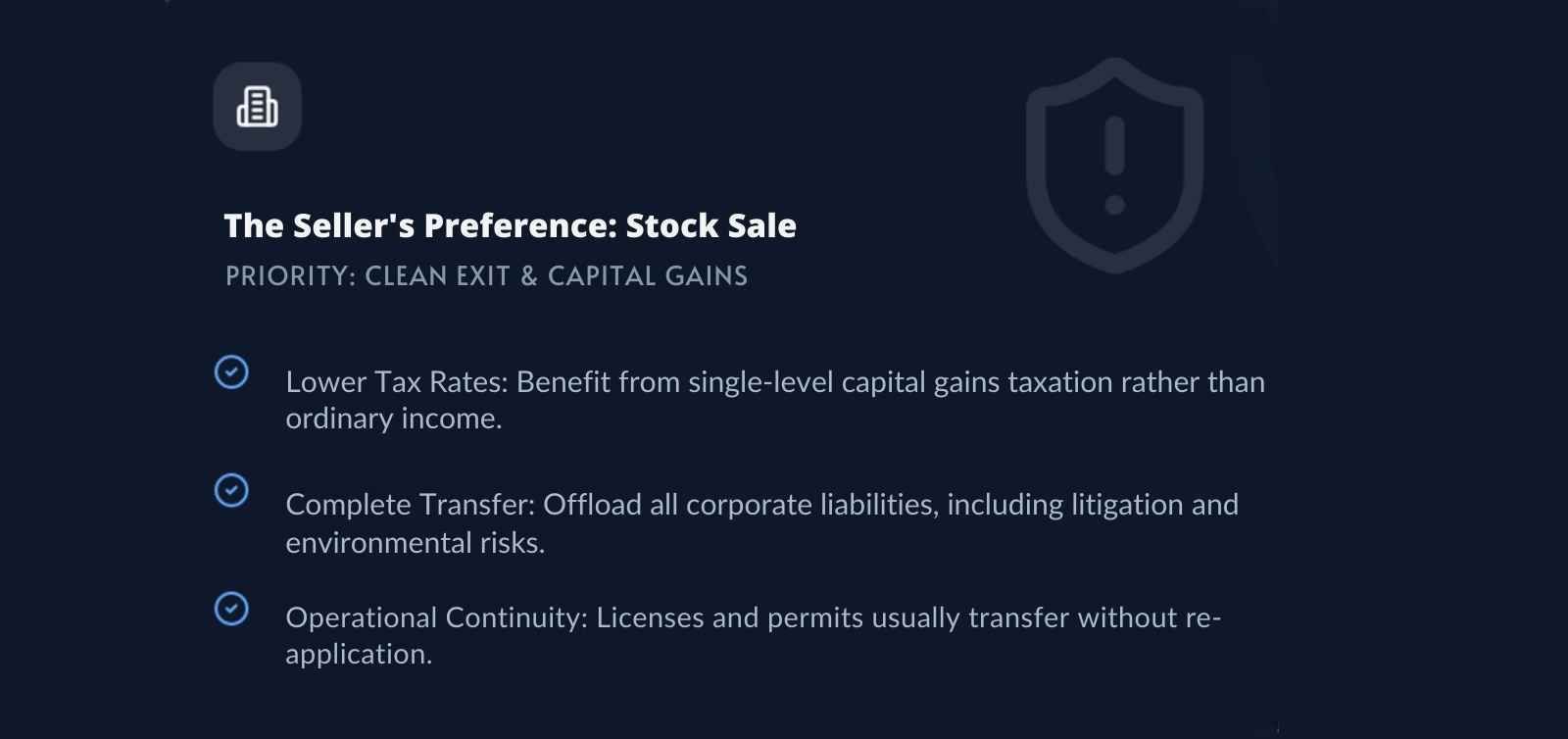

| (Taxation) Tax Treatment (Seller) | Potential Double Taxation (C-Corp) | Single-level Capital Gains |

| (Legal) Liabilities | Buyer "cherry-picks" assets | Buyer inherits all baggage |

| (Operational) Contracts & Licenses | Requires new titles/assignments | Automatically transfer (usually) |

| (Taxation) Depreciation | Higher (from stepped-up basis) | Lower (continues historical) |

Strategic M&A Tax Implications:

The Step-Up Advantage Explained

Tax Amortization of Goodwill

In an asset sale, the purchase price exceeding the book value (Goodwill) can be amortized over 15 years, significantly lowering the buyer's future tax burden.

Successor Liability Doctrines

While asset sales shield from many risks, "Successor Liability" laws in states like California can still hold buyers liable for unpaid employment taxes or environmental claims.

M&A Deal Structure FAQs

What is a Section 338(h)(10) election?

It is a tax election that allows a stock sale to be treated as an asset sale for federal tax purposes. This provides the buyer with a 'basis step-up' while allowing the seller to execute a stock transfer.

Why do sellers fear asset sales?

Primarily because of double taxation in C-Corporations (tax at the corporate level on the sale, then tax at the individual level on distribution) and the risk of being left with 'excluded' liabilities.

Which deal structure is faster to close?

Generally, stock sales are faster because they don't require re-titling every individual asset or obtaining third-party consents for every contract assignment.

Ready to Structure Your Next

Multi-Million Dollar Deal?

Strategically updated for 2026 M&A and Tax Guidelines.

California Specific Warning

DRE Licensing Enforcement

To value and sell a business in CA, the firm must hold a California Department of Real Estate license. Unlicensed out-of-state "free" tools are illegal in CA.

Board Compliance (CSLB/BAR/ABC)

Free estimates ignore California's complex licensing clearances. Buying a construction or auto repair shop without CSLB/BAR clearance can trigger immediate legal failure.

Negotiate from Strength, Not Guesswork.

"If your business is in California, an out-of-state free business valuation is the fastest way to lose millions in structural errors. We live and breathe CA M&A."

Specialization Matters

Rogerson Business Services handles the Lower Middle Market (Gross Revenue $2M–$100M) with a track record of closing complex transactions across multiple CA sectors.

Request Your Defensible Analysis

For serious business owners ready to exit.

All reports are signed by a licensed principal.