The 7 Pillars of Lower Middle Market Business Valuation (2026 Guide)

Lower Middle Market Business Valuation

By: Rogerson Business Services (California lower middle-market M&A advisory)

About the author/firm: Rogerson Business Services advises owners of $2M–$50M revenue businesses in California on valuation, sell-side M&A execution, and exit planning.

Profiles: CABB · IBBA · M&A Source · Axial · About

Last updated: April 2026

Privacy: If you contact us through this page, we handle your information per our Privacy Policy.

Lower Middle Market Business Valuation is where many owners first encounter the “valuation gap”: the difference between what a founder believes the business is worth and what a sophisticated buyer will underwrite.

In practice, this gap shows up most clearly between Main Street transactions (often priced off “owner cash flow”) and the lower middle market (LMM)—typically defined as businesses with roughly $5M–$50M in revenue where buyers expect institutional reporting, diligence-ready financials, and a forward-looking value creation plan.

In 2026, valuation is no longer a “multiple of the past.” It is a projection of the future—discounted for risk, adjusted for credibility, and stress-tested in due diligence.

Key Takeaway: The best valuation outcomes in 2026 are rarely “negotiated.” They are prepared—through clean earnings, defensible forecasts, and reduced diligence friction.

Disclaimer: This article is for educational purposes only and is not financial, tax, or legal advice. Consult qualified professionals for advice specific to your situation.

1. The EBITDA Standard: Moving Beyond SDE in Lower Middle Market Business Valuation

The first step in lower middle market business valuation is agreeing on the earnings base.

In smaller transactions, valuation often relies on SDE (Seller’s Discretionary Earnings)—a measure of owner benefit that adds back discretionary expenses and the owner’s compensation because a buyer is typically stepping into the owner-operator role.

In the LMM, buyers usually shift to EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) because it is more comparable across companies and capital structures—and it aligns better with how lenders and institutional buyers think about cash flow.

The 2026 normalization reality

“Normalization” is not a creative exercise. It is the process of converting historical financials into a sustainable, defensible earnings level a buyer can underwrite.

Common normalization categories include:

- One-time legal, relocation, or restructuring costs (if they truly won’t recur)

- Owner compensation adjusted to market (especially when family members are on payroll)

- Discretionary expenses that are not required to run the business

- Revenue or margin anomalies that won’t repeat (positive or negative)

In 2026, the question is less “can you argue an add-back?” and more “can it survive a buyer’s verification process?” That is where many valuations break.

EBITDA Multiples 2026: median ranges by sector (illustrative)

Multiples vary by deal size, growth rate, customer concentration, and the credibility of the earnings base. Still, owners benefit from seeing “typical” bands to calibrate expectations.

| Sector | Typical LMM EV/EBITDA Range (2026) | What drives the high end |

|---|---|---|

| Manufacturing / Industrial | 5–7x | diversified customers, documented processes, capex discipline, management depth |

| SaaS / Software | 10–15x | durable ARR, low churn, high gross margin, credible growth engine |

| Healthcare Services | 8–10x | payer mix stability, compliance maturity, provider depth, recurring demand |

These ranges should be treated as starting points, not promises. For market-wide context, GF Data’s 2025 reporting placed average middle-market purchase price multiples around ~7x and showed quarter-to-quarter movement consistent with a volatile underwriting environment (see GF Data “Q4 2025 M&A and Leverage Reports” (ACG, 2026) and Mercer Capital “Middle Market Transaction Update — Spring 2026” (2026)).

If you want a California-specific primer on methodology and preparation, see Business Valuation Guide for California Lower Middle Market Owners.

2. The Income Approach: DCF in a Volatile 2026 Market

When markets are choppy, buyers lean more heavily on the income approach, especially Discounted Cash Flow (DCF).

DCF is conceptually simple: you forecast future free cash flows, then discount them back to today using a required rate of return. The complexity is not the math—it is the realism of the assumptions.

How WACC is built in 2026 (in plain English)

The discount rate is often anchored to WACC (Weighted Average Cost of Capital)—a blended cost of equity and after-tax cost of debt.

At a high level, WACC reflects:

- A risk-free baseline (often tied to U.S. Treasury yields)

- An equity risk premium (the extra return investors expect for equities)

- Business-specific risk (size, customer concentration, cyclicality, management depth)

- The after-tax cost of debt (which matters more when rates are elevated)

In 2026, this matters because the market is re-pricing risk more explicitly. A business with the same EBITDA can carry a very different discount rate depending on how “financeable” it is.

Expert commentary:

“A DCF is only as strong as its terminal value assumptions. Over-optimism here is where most LMM deals die during due diligence.”

If you’re building a DCF for a sale process, the goal isn’t to “win the spreadsheet.” It’s to produce a forecast a buyer can accept without re-trading.

3. Case Study: The $34M Industrial Manufacturing Exit

Consider a hypothetical—but realistic—manufacturing M&A case study: the sale of Apex Precision Engineering, an industrial manufacturer with an IoT-enabled CNC line.

Apex is profitable, but not perfect:

- Solid EBITDA history

- Capable engineering team

- Growth tied to a few key accounts

- An operations story that is improving, but still founder-influenced

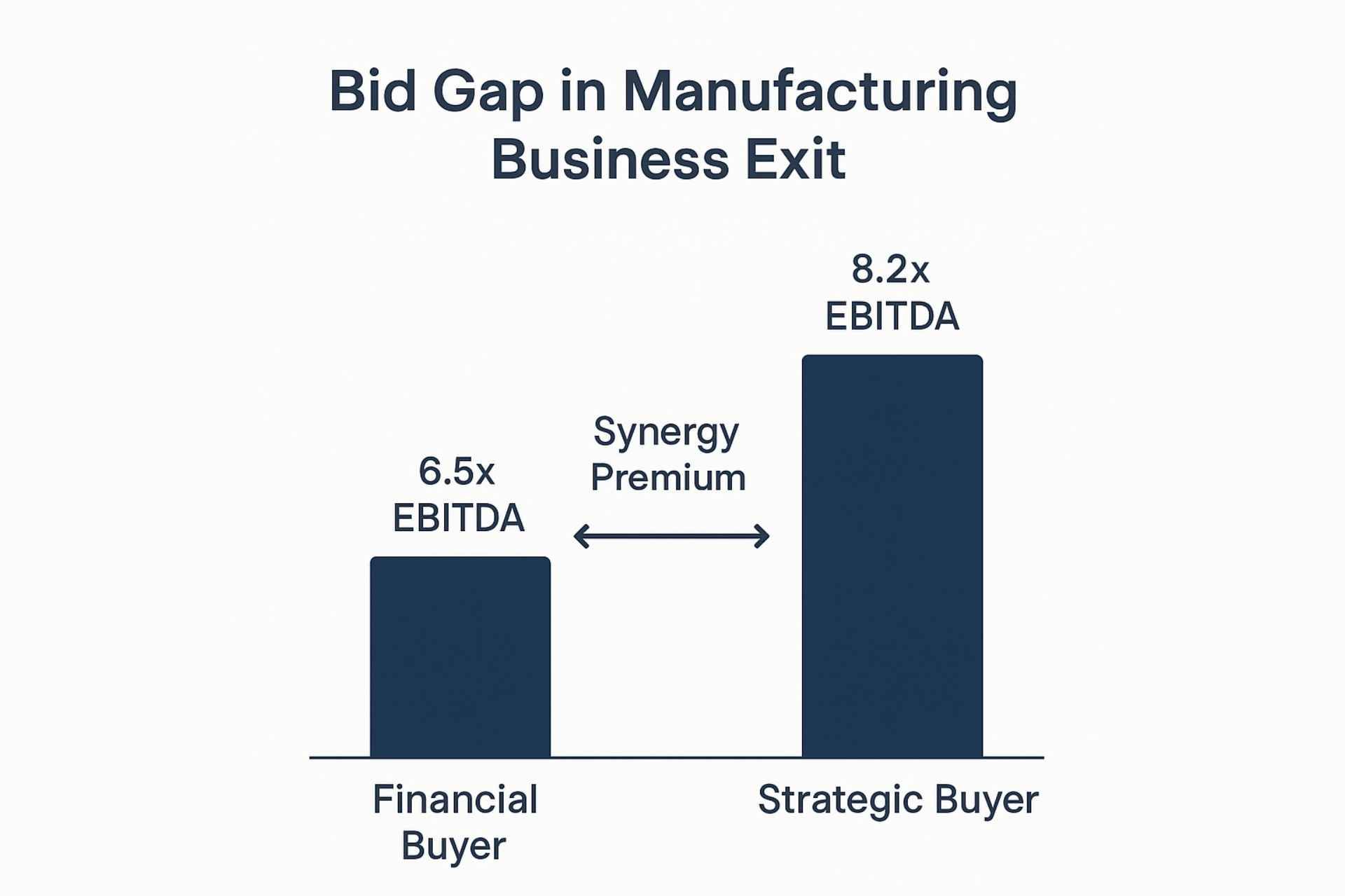

Strategic vs. Financial Buyers: why the same EBITDA gets different bids

A financial buyer (typically private equity) underwrites value based on:

- cash flow durability

- downside protection

- financing terms

- a credible path to operational improvements

A strategic buyer (often a competitor or adjacent operator) can justify paying more if they see synergies—cost savings or revenue expansion created by combining businesses.

In this example:

- Financial buyer bid: 6.5x EBITDA

- Strategic buyer bid: 8.2x EBITDA

The difference is the synergy premium. The strategic buyer believed Apex’s IoT-enabled CNC line would accelerate throughput and reduce scrap across the combined footprint—a value that would not exist for a standalone financial sponsor.

The practical lesson for owners is not “find a strategic buyer.” It is: build a buyer-specific value story. Strategic vs. financial buyers do not value the same facts the same way.

For manufacturing owners thinking about readiness, a useful next reference is the Guide to Selling a Manufacturing Business in California.

4. The Quality of Earnings: The “Shield” of Valuation

In 2026, Quality of Earnings (QofE) is no longer optional for many deals. It is the tool that separates a headline valuation from a defensible valuation.

A QofE is not an audit. It is a forensic review of how sustainable earnings really are—how repeatable revenue is, how reliable margins are, and which adjustments are credible.

Revenue concentration and the valuation haircut

If a single customer represents more than ~15% of revenue, sophisticated buyers often price in concentration risk.

They may do it through:

- a lower multiple

- a larger escrow/holdback

- an earnout structure

- or a strict working capital peg

The mechanism varies. The outcome is similar: earnings are discounted because the revenue stream is not fully “owned” by the business.

Add-back verification: where deals get re-traded

Most founders understand add-backs conceptually. The failure mode is verification.

Add-backs that often get challenged:

- “one-time” expenses that recur annually

- personal expenses routed through the business that lack clear documentation

- family payroll that is not truly removable

- deferred maintenance that will become post-close capex

⚠️ Warning: Aggressive add-backs may inflate the teaser valuation, but they also increase the odds of a late-stage re-trade—exactly when you have the least leverage.

Soft next step: Get the “QofE Preparation Guide” for LMM founders (a practical checklist of what buyers verify, and how to document it).

5. The “AI Alpha”: Valuing the Modern Tech Stack

In 2026, buyers are paying attention to “AI readiness”—but not in the way most owners expect.

The premium is not for saying “we use AI.” The premium is for measurable operational advantage and a tech stack that can support scalable decision-making.

AI-washing vs AI-integration

AI-washing looks like:

- a generic chatbot on the website

- loose claims about “automation” with no operational baseline

- ad hoc tools that live in one person’s workflow

AI integration looks like:

- predictive maintenance on equipment (reduced downtime)

- improved procurement through demand forecasting (lower expediting costs)

- production scheduling that reduces changeover time

- tighter QA analytics that reduce scrap or warranty exposure

In buyer terms, AI integration is valuable because it creates repeatable margin improvement and reduces key-person dependency.

6. Asset-Based Valuation: The Floor and the Ceiling

Asset-based valuation is not the primary method for most profitable LMM businesses—but it often establishes the floor.

It becomes central when:

- earnings are volatile or depressed

- the company is asset-heavy (manufacturing, industrial services)

- liquidation value matters (distress, recapitalizations)

- “cost to recreate” is the buyer’s real alternative

Cost to recreate (and why it matters)

If a buyer believes they can replicate your capabilities, equipment, certifications, workforce, and process know-how faster and cheaper than buying you, your valuation ceiling compresses.

Manufacturing note: FMV-ICU for machinery & equipment

For machinery and equipment (M&E), appraisals sometimes use Fair Market Value in Continued Use (FMV-ICU)—value assuming the assets remain installed and productive in their current operating context.

A plain-English definition is provided in BDC’s “Equipment valuation: How to do it” (updated 2026).

7. The Pre-Exit Readiness Checklist

If you want to reduce the valuation gap, treat valuation like an operational project with an 18-month runway.

Here is a practical checklist to begin 18 months before a sale:

- Clean up the balance sheet (remove non-operating assets; document unusual liabilities).

- Tighten monthly financial reporting cadence (close within 15–20 days; explain variances).

- Normalize owner compensation and related-party arrangements.

- Reduce customer concentration where possible (or secure longer-term agreements).

- Document pricing logic and margin drivers by product line or customer segment.

- Phase out the founder-centric sales model; build a repeatable pipeline and delegation.

- Lock in key managers with retention plans (and clarify roles post-close).

- Secure long-term contracts where feasible; expand recurring revenue elements.

- Build a data room early (contracts, HR, IP, leases, compliance, capex history).

- Identify the top 5 diligence issues you already know exist—and fix them before a buyer finds them.

Next steps (when you’re in the window)

If you are a manufacturing owner preparing for a sale, two evaluation lenses matter as much as the headline multiple: deal certainty and risk-adjusted, after-tax proceeds.

A useful framing is the concept of Risk-Adjusted Net Proceeds: a lower nominal offer can outperform a higher headline price once you account for structure, taxes, and probability of payout.

Request a Confidential Valuation Analysis for your Manufacturing Business.

About the Author

Andrew Rogerson is an M&A advisor with 20+ years of mergers and acquisitions experience working with owner-led businesses. His qualifications include Certified Mergers & Acquisition Professional (CM&AP) and Mergers & Acquisition Master Intermediary (M&AMI) designations from M&A Source, a Certificate in Private Capital Markets (CIPCM) from Pepperdine University, and the Certified Business Intermediary (CBI) credential.

Rogerson Business Services supports California founders with confidential, ethical sell-side M&A advisory and valuation work. (RBS Advisors)

Hey there! Can we send you a gift?

We just wanted to say hi and thanks for stopping by our little corner of the web. :) we'd love to offer you a cup of coffee/tea, but, alas, this is the Internet.

However, we think you'll love our email newsletter about building value and properly position your company before transition/exit your business ownership.

As a special welcome gift for subscribing, you'll also get our helping and educational guides, tips, tutorials, etc.. for free.

It's filled with the best practices for retiring serial business owners like Dan Gilbert, Larry Ellison, Warren Buffett, and many more.

Just sign up for our emails below.