Business Valuation Guide For California Lower Middle Market Owners

Business Valuation Guide Made Simple For Biz Owners

By Andrew Rogerson, CM&AP, LCBB (Rogerson Business Services).

Andrew Rogerson is an M&A advisor and a 35+ year business owner who helps California lower and mid-market owners value, position, and sell their companies through sell-side representation—credentials: CM&AP and LCBB listing.

You've spent decades building your California business, and now you're ready to exit within the next few years. But how much is your company actually worth?

For lower middle market owners with $2M to $50M in annual revenue, determining a defensible valuation is the critical first step toward a successful sale. This guide walks you through proven valuation methodologies, California-specific tax considerations, and practical preparation steps that position you for a high-value exit.

Key Takeaways

| Point | Details |

|---|---|

| Triangulate valuation methods | Use income, market, and asset based approaches to establish a defendable price range. |

| Gains taxed ordinarily | California taxes capital gains as ordinary income up to 13.3 percent, which can substantially impact after tax proceeds. |

| Plan 12 to 24 months | Start preparing 12 to 24 months ahead for a smooth exit process. |

| Clean finances diversify client base | Cleaning financials and diversifying the client base can improve valuation multiples. |

| Benchmark against peers | Use comparable company data and industry benchmarks to validate your valuation range and strengthen negotiations. |

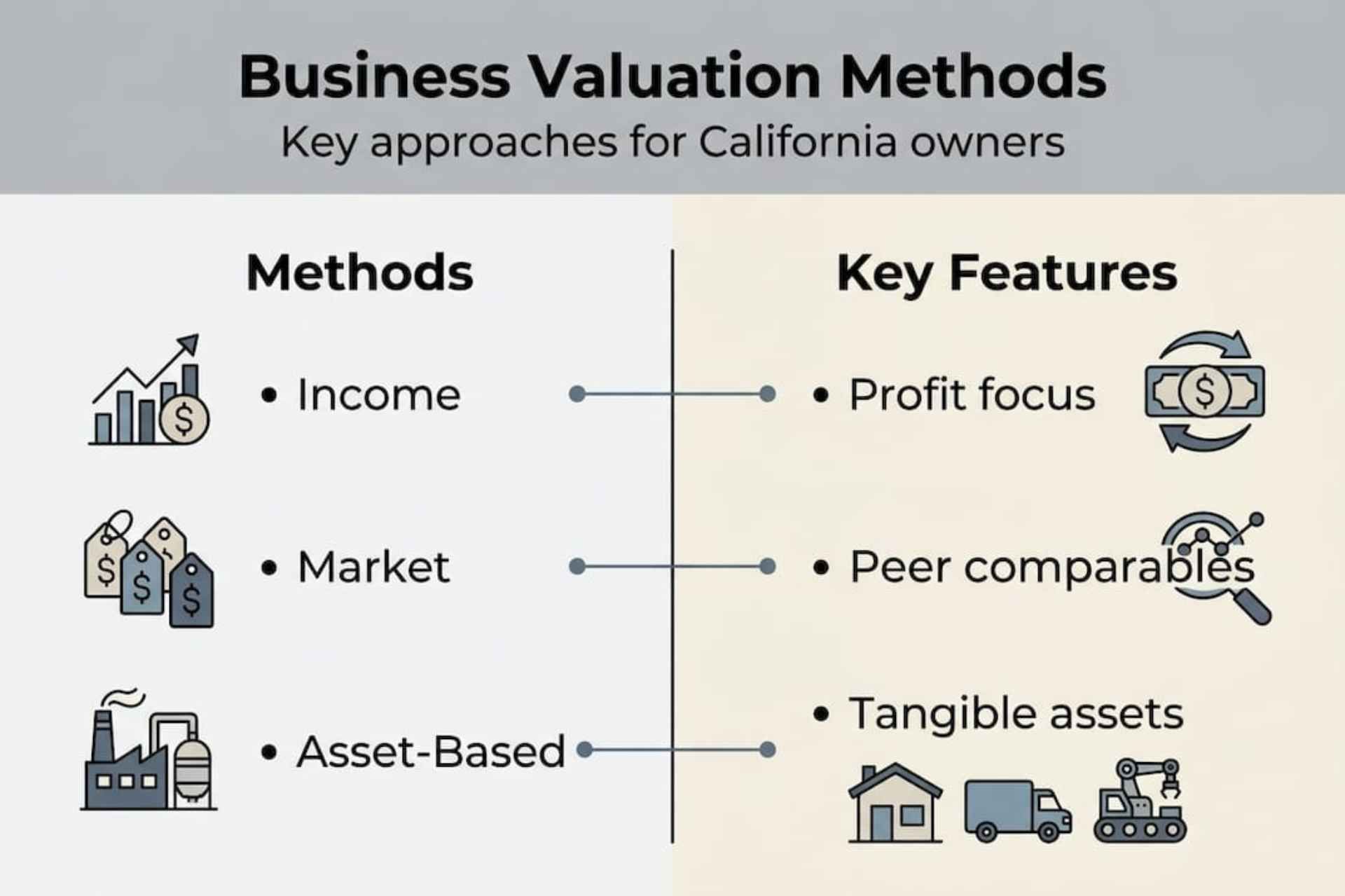

Understanding core valuation methodologies

Valuing a lower middle market business requires a structured approach that combines multiple methodologies to establish a credible price range. The three primary methods are the income approach, market approach, and asset-based approach, each offering unique insights into your company's worth.

The income approach focuses on your business's earning power. EBITDA multiples typically range 4 to 12x for middle market businesses, while owner-operated companies often use Seller's Discretionary Earnings multiples of 2.5 to 3.5x. This method also includes discounted cash flow analysis, which projects future earnings and discounts them to present value, and capitalization of earnings, which divides normalized earnings by a capitalization rate. The key is normalizing your earnings by adding back owners' personal expenses, one-time costs, and discretionary spending to show true profit potential.

The market approach compares your business to similar companies that have sold recently or are publicly traded. You can use comparable company analysis to benchmark against peers or review precedent transaction data from your industry. However, private middle market transaction data is often sparse, making this method challenging to apply in isolation. When reliable comparables exist, they provide powerful validation of your valuation range.

The asset-based approach calculates the adjusted net value of your company's assets minus liabilities. This method works best for asset-heavy businesses like manufacturing or distribution companies. You adjust book values to fair market value, accounting for equipment depreciation, real estate appreciation, and intangible assets such as customer relationships and intellectual property.

Core valuation methodologies include income, market, and asset-based approaches for firms with $2M to $50M in revenue, triangulated for a defensible valuation. Relying on a single method creates vulnerability in buyer negotiations. Smart sellers use all three to establish a range, then defend that range with normalized financials and industry benchmarks.

Pro Tip: Create a comparison table showing each valuation method's results, key assumptions, and applicable scenarios. This visual tool strengthens your position during negotiations by demonstrating thorough analysis.

Comparison of valuation methodologies

| Method | Best use case | Key strength | Primary limitation |

|---|---|---|---|

| Income approach (EBITDA multiples) | Service businesses, consistent cash flow | Reflects earning power and buyer ROI expectations | Requires reliable historical earnings |

| Market approach (comparables) | When similar transactions exist | Grounds valuation in real market activity | Private company data often unavailable |

| Asset-based approach | Manufacturing, real estate-heavy firms | Provides floor value based on tangible assets | Undervalues goodwill and earning potential |

Don't have time to read more?

Take a shortcut and play the video overview below

Understanding business valuation formulas and business valuation methods helps you speak confidently with buyers and advisors. For deeper insights into private company valuation methods, explore comprehensive frameworks that address your specific business model.

California-Specific Tax and Legal Considerations For Business Valuation and Exit

California's tax and regulatory environment significantly impacts your net sale proceeds and exit timeline. Understanding these factors early helps you structure the deal optimally and avoid costly surprises.

Capital gains from business sales in California are taxed as ordinary income up to 13.3%, one of the highest state rates in the nation. Combined with the federal capital gains tax, your total tax burden can exceed 30% of the sale price. This makes after-tax modeling essential. Many sellers prefer asset sales because they allow buyers to step up the tax basis of acquired assets, creating depreciation benefits that justify higher purchase prices. However, asset sales can trigger higher taxes for C corporation sellers, requiring careful analysis of your specific entity structure.

California's Bulk Sale Act and escrow requirements add complexity and time to transactions. Boomers aged 50+ increasingly seek exits, requiring 12 to 24 months planning amid escrow and Bulk Sale Act compliance. Escrow periods typically extend 30 to 60 days beyond standard closing timelines, during which title searches, lien releases, and regulatory filings must be completed. The Bulk Sale Act requires sellers to notify creditors before transferring business assets, protecting creditors but adding administrative burden.

For business owners over 50, health considerations and retirement planning often create urgency to exit. However, rushing the process usually costs you money. Buyers detect desperation and negotiate harder. California's regulatory environment rewards patient, methodical preparation.

Pro Tip: Model your net proceeds under multiple scenarios: asset sale vs stock sale, different earnout structures, and varying tax years. Small timing and structure changes can save hundreds of thousands in taxes.

"California's combined state and federal capital gains tax can consume over 30% of your sale proceeds. Strategic structuring and timing decisions made 18 months before closing often determine whether you keep an extra $500,000 or more."

Understanding the asset sale vs stock sale comparison helps you negotiate structure intelligently. Familiarize yourself with California business valuation laws and California business sale regulations to avoid compliance pitfalls that delay or derail your exit.

- California taxes capital gains as ordinary income, not at preferential rates

- Asset sales are often preferred by buyers but may increase the seller's tax burden

- Escrow and Bulk Sale Act compliance adds 30 to 60 days to closing timelines

- Entity structure (LLC, S corp, C corp) dramatically affects tax treatment

- Early tax planning with a CPA specializing in business sales is essential

Preparing Your Business For a Higher Valuation in California

Preparation directly determines the price that multiple buyers will pay. Cleaning financials, client diversification, and process documentation can increase valuation multiples by 1 to 2x. The difference between a 4x and 6x EBITDA multiple on a business with $2M in earnings is $4M in sale price.

Start by getting your financial house in order. Buyers scrutinize three years of financials, tax returns, and internal management reports. Discrepancies between these documents raise red flags and kill deals. Work with your CPA to create clean, normalized financial statements that add back the owner's salary above market rates, personal expenses run through the business, one-time legal costs, and discretionary spending. These add-backs demonstrate true earning potential.

Client concentration is a major valuation killer. If your top three clients represent over 40% of revenue, buyers will heavily discount your price or walk away entirely. Start diversifying 18 to 24 months before selling. Add new clients, expand services to existing smaller clients, and document contract renewals to show relationship stability.

Process documentation proves your business can operate without you. Create standard operating procedures for key functions, document vendor relationships and pricing, maintain updated employee handbooks and org charts, and systematize customer acquisition and service delivery. Buyers pay premiums for businesses that won't collapse when the owner leaves.

Five key preparation steps for maximizing business valuation:

- Normalize and clean three years of financial statements with clear add-back schedules

- Reduce client concentration below 30% for the top three customers

- Document all critical business processes in written SOPs

- Develop management depth by delegating key responsibilities

- Address deferred maintenance on equipment, facilities, and technology systems

Pro Tip: Owner dependency is one of the largest valuation discounts. Start transitioning daily operations to a management team 12 to 18 months before listing your business. Buyers will pay significantly more when they see the business runs smoothly without constant owner involvement.

Review preparation steps for sale and business sale preparation tips for industry-specific tactics that boost buyer confidence and valuation multiples.

Executing a defensible valuation and planning your exit strategy

Once you've prepared your business, executing a defensible valuation requires combining methodologies into a coherent story that withstands buyer scrutiny. Triangulate income, market, and asset approaches to develop a defensible valuation range for exit negotiations. This triangulation gives you confidence and credibility when buyers challenge your asking price.

Start by calculating your business value using each method independently. Apply industry-appropriate EBITDA multiples to your normalized earnings, research comparable sales in your sector and geography, and determine adjusted net asset value if applicable. When all three methods cluster around a similar range, you have a strong valuation. If they diverge significantly, investigate why and adjust your approach.

Prepare to justify every assumption. Buyers will question your add-backs, challenge your multiple selections, and scrutinize growth projections. Document why each add-back is legitimate, how you selected your EBITDA multiple based on industry data, what comparable transactions support your range, and how you've addressed concentration and dependency risks. This preparation turns negotiations from emotional arguments into data-driven discussions.

Timing your exit properly maximizes value. Plan 12 to 24 months ahead to complete preparation tasks, accommodate due diligence periods of 60 to 90 days, and navigate California's regulatory requirements. Rushing creates leverage for buyers who sense desperation.

Steps for defending valuation and conducting exit negotiations:

- Calculate value using income, market, and asset methods independently

- Document all assumptions with industry data and comparable transactions

- Prepare detailed add-back schedules with supporting receipts and explanations

- Create a data room with organized financials, contracts, and operational documents

- Engage an experienced M&A advisor or business broker familiar with California regulations

- Model multiple deal structures to understand tax implications before negotiations

EBITDA multiples by industry for lower middle market businesses:

| Industry sector | Typical EBITDA multiple range | Key value drivers |

|---|---|---|

| Professional services | 4.5 to 7.0x | Client retention, recurring revenue, low capital needs |

| Manufacturing | 4.0 to 6.5x | Equipment condition, customer diversity, proprietary processes |

| Distribution | 3.5 to 5.5x | Supplier relationships, logistics efficiency, inventory management |

| Technology/SaaS | 6.0 to 10.0x | Recurring revenue, growth rate, customer acquisition cost |

| Healthcare services | 5.0 to 8.0x | Regulatory compliance, payor mix, staff retention |

Expect buyers to request adjustments for owner dependency if you're still central to operations, client concentration if top customers represent over 25% of revenue, and deferred capital expenditures that the buyer must fund post-closing. Address these issues during preparation rather than negotiation.

Explore the comprehensive business valuation guide overview for additional frameworks and tools that support confident exit execution.

Achieve your successful business exit in California

Navigating a lower middle market business sale in California requires specialized expertise in valuation, tax planning, and regulatory compliance. You've invested decades building your company, and maximizing your exit value demands the right support.

Mid Market Businesses offers business valuation services tailored specifically for California owners with $2M to $50M in revenue. Our team understands the unique challenges you face and provides defensible valuations that withstand buyer scrutiny. Ready to connect with qualified buyers? List your business for sale in California on our platform, where serious acquirers actively search for businesses like yours. Download our business for sale listing guide to learn how to position your company for maximum buyer interest and optimal pricing.

Frequently Asked Questions

What is the best method to value a lower middle market business?

Triangulating income, market, and asset-based methods offers the most reliable valuation range for lower middle market businesses. Single methods alone may miss nuances unique to your business or industry. Using all three provides credibility in negotiations and helps you defend your asking price with data.

How does California's capital gains tax affect my business sale?

California taxes capital gains up to 13.3% as ordinary income, significantly impacting net sale proceeds. Combined with federal taxes, your total burden can exceed 30% of the sale price. Proper planning and modeling net proceeds under different deal structures helps optimize your exit strategy and maximize what you keep.

What should I do to improve my business valuation before selling?

Clean and normalize your financial statements to show true earning potential. Diversify customers to reduce concentration risk below 30% for your top three clients. Document key business processes to demonstrate operational stability and transferability. These steps can increase your valuation multiple by 1 to 2x.

How long does it typically take to prepare and exit a business in California?

Plan for a 12 to 24 month timeline due to preparation tasks, legal requirements, and escrow compliance. California's Bulk Sale Act and regulatory environment add 30 to 60 days beyond standard closing periods. Early planning mitigates risks, addresses valuation discounts, and ensures a smoother sale process that maximizes your proceeds.

ibe the item or answer the question so that site visitors who are interested get more information. You can emphasize this text with bullets, italics or bold, and add links.

Hey there! Can we send you a gift?

We just wanted to say hi and thanks for stopping by our little corner of the web. :) we'd love to offer you a cup of coffee/tea, but, alas, this is the Internet.

However, we think you'll love our email newsletter about building value and properly position your company before transition/exit your business ownership.

As a special welcome gift for subscribing, you'll also get our helping and educational guides, tips, tutorials, etc.. for free.

It's filled with the best practices for retiring serial business owners like Dan Gilbert, Larry Ellison, Warren Buffett, and many more.

Just sign up for our emails below.